TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

An Rv is not just a luxury vehicle, but a home on wheels. During your tours in Fisherville, KY, many things can happen, including a road accident. Have you figured out how much loss that would be if you didn’t have any form of insurance?

Well, Rvs are pretty expensive. On top of that, they carry your valuables just like home. Speaking to an insurance expert in TruePoint Insurance can be a great idea as we will help you find out how much coverage is adequate for you.

Why do you need RV insurance?

We have already mentioned that RVs are like our homes on wheels, which means they carry a lot of value on the roads as well as when packed. While many states do not require drivers to have RV insurance, it makes sense to have a substantial amount of coverage in case anything happens to you out there. While they require ordinary driving skills, Rvs are bigger cars. You will need to make accurate estimations when driving or packing.

Factors that impact Rv insurance premiums

While insurance rates are different for every Rv owner, insurance companies use various criteria to calculate based on the information that you provide. Providing truthful information is a requirement as failure to do so can result in fines. Your Rv insurance premiums will be calculated based on the following factors:

The size of your RV

The age of the RV

Whether you are living in it or not

How long you will be using your Rv

Where you pack or store your Rv when not in use

Your location/address and many more

Your RV is a huge investment that needs to be protected at all costs. Large vehicles can cause significant damages and injuries to the parties involved. You don’t want to risk taking a tour in an uncovered car.

Do you need help buying Rv insurance? TruePoint Insurance can arm you with the right information to help you make a wise decision. Visit us at Fisherville, KY today.

Mobilehomes are vulnerable to serious damage from winds and storms since they are smaller and much lighter than stick-built or factory built homes. It is important to use reinforcements to make them more stable; such as tiedowns.

Tiedowns come in two basic types; over-the-top tiedowns and frame anchors. Over-the-top tiedowns are straps that resist lifting forces and minimize tipovers. They are usually used with single-wide mobilehomes. Strapping is placed with over the top of the roof or over the structure’s sides. Frame anchors are reinforcements that resist lateral forces, making a structure less vulnerable to sliding off supports

In order to stabilize a structure, the tiedowns must be properly anchored to a foundation, slab or the ground. Anchor types include the following:

· Hard Rock Anchor

· Concrete Slab Anchor

· Cross Drive Rock Anchor

· Drive or Barb Anchor

· Auger Anchor

· Disc Anchors

Straps and anchors have to be used properly and they have to meet various standards such as placement of anchors, anchor fittings, method of installation and ground/site conditions. When anchored to the ground, it may be necessary to make test its suitability as an anchor. If piers and footings are used they must be able to meet various requirements regarding weight support, dimensions, material quality, pier placement and other areas. Straps and anchors also have to meet requirements in order to be depended on to withstand the stresses winds and other forces.

Use of tiedowns varies by state, state regulations and soil type. Local building inspectors and mobile and manufactured home builder associations are excellent sources for anchoring and tiedown requirement information. Use of that valuable information, along with insurance, is great methods for fully protecting a mobilehome.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Learn about flood insurance before the waters start to rise.

Who needs flood insurance? Many residents of Georgia and South Carolina are exposed to flood risk. Those living in coastal areas are like to be more at risk. Consider the following:

River Road – It seems wise that anyone living on River Road should check in to flood insurance.

Coastal Highway – Another great clue that suggests there is a heightened risk for flooding.

Lowcountry– Since floods occur in low lying area, it’s probably wise to consider flood insurance if you live in a region known as the Lowcountry.

Anyone with Lender Requirement

Does your home mortgage require flood insurance?

Your homeowner’s policy does not protect against flooding. For anyone needing protection from rising waters, a separate Flood Insurance policy is required. This policy will provide specific coverage if your home is damaged by a local flood.

Residents in Coastal Georgia and South Carolina may find that they are required to purchase flood insurance. This requirement is most likely come for a lender. Mortgage lenders know the potential impact of floods as well as which homes are at greatest risk. Due to this risk, borrowers with homes located in a FEMA identified flood zone will likely be required to maintain flood insurance.

Needs to Cover Against Risk

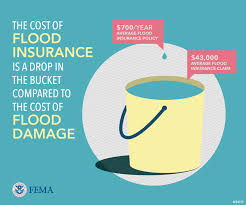

Flood Loss versus Cost. You do the math!

FEMA flood zones are divided into one of many categories. These categories or buckets identified the flood risk as very risky or a Special Flood Hazard Area (SFHA). Somewhat lower-risk areas are considered Moderate Flood Hazards. There are two moderate flood hazard groups; Zone B and Zone X (Shaded). Finally, the areas that are exposed to potential flooding yet have the least risk are identified as minimal flood hazards. This grouping also has twp categories; Zone C and Zone X (Unshaded)

Even if the risk is small, you should still consider getting flood insurance. Everyone should consider buying flood insurance. This includes those without a mortgage, and those not required to have flood insurance.

When you are looking to learn more about flood insurance in Georgia or South Carolina, you should speak with the team at TruePoint Insurance. They will make work hard to make sure that your decision is as simple as possible.

Understanding Mobile and Manufactured Home Insurance

Insurers commonly provide coverage for mobile/manufactured homes by modifying a conventional homeowner policy with provisions called endorsements. The endorsements change key definitions and other elements of a conventional policy to fit a mobile or manufactured home situation. The result is a modified homeowner package that protects the home, outbuildings (unattached garages, sheds, etc.) and personal property. They also provide insurance for personal liability. Regardless of the type of home you own or live in, it is important that you learn about the coverage options that are available. You may find that different policies vary considerably in coverage and price.

Coverage for mobile/manufactured homes is generally offered using two approaches. Some policies include a laundry list of items (or perils) that may cause a loss. Other policies protect your home against everything EXCEPT for a host of specified perils. Either approach includes liability coverage that protects you for injuries or losses to others which you accidentally cause.

Property Insurance Needs

Mobile, Modular, or Manufactured? Insurance need to Know.

Any coverage option you choose is likely to reflect the fact that mobile homes are, well, mobile. Therefore coverage is affected by the fact that mobile homes:

are able to move under their own power (or are capable of being easily transported);

are more susceptible to wind damage,

tend to lose value with age.

The mobility of such homes creates a special need to protect the financial interest of the business that lent the money to purchase the home. For example, a mobile home owner who lives in Ohio decides to drive his home to Arkansas. The soon-to-be Arkansas resident “forgets” to mention his plan (and his new address) to his Ohio Mortgage Company. The Ohio lender would be out of luck if the policy didn’t include protection for this whimsical act. Another way in which a mobile or manufactured homeowner policy differs from conventional homeowner coverage involves coverage for unattached buildings. This coverage is usually minimal for, say, $2,000. Such a provision helps keep the premiums for policies lower by avoiding paying claims on very low value structures. The coverage is likely to be offered on an actual cash value basis. Unfortunately, mobile and manufactured homes tend to lose value over time.

The policy is likely to include a provision that requires you to get permission to move your home. Once granted, you’re likely to get thirty days of special transportation protection for collision; sinking, upset or stranding (a special, higher deductible may apply during the move). Another common coverage feature is coverage for your attempt to move the home in order to prevent damage from an insured cause of loss. For example, you move your mobile home fifty feet to get away from a neighboring trailer that is on fire. IMPORTANT: coverage for moving endangered property usually has a modest limit (several hundred dollars is typical) because of owners who may be too heroic or clumsy for anyone’s good.

Liability Insurance Needs

The liability protection connected with mobile or manufactured homes is, for all practical purposes, identical to the liability provided to conventional home owners. Why? The likelihood of guests to be hurt at your home, or your probability of being sued, tends to be the same. The important thing to remember is that your agent is a tremendous source for getting the information you need to be sure that your home and property are adequately protected at a reasonable price.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions