TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

The Commercial General Liability policy leaves several

liability exposures for contractors. The

General Liability policy doesn’t cover faulty work due to negligence, or to

damages to the work of the contractor.

Contractors E&O has been already, but until recently,

only limited options existed.

Contractors now have access to reasonably priced insurance that closes

some very significant gaps.

If your business has never had to turn in an insurance claim many will tell you to consider yourself lucky. Others may tell you to give yourself a pat on the back. At TruePoint, we will tell you that it is highly likely that both are true.

No one enjoys turning in an insurance claim. Once we get past the fact that no one is injured, an explosion of thoughts race through our minds. How much is this going to cost? What’s my deductible? How much will my insurance premium go up? Will I get canceled?

The one thought that is seldom considered is, “will my insurance company deny the claim?” Most small businesses seldom consider needing anything more than a General Liability policy. If you are a contractor that has had a past claim denied, then you most likely know where we are headed.

General Liability Insurance or GL covers a boatload. Even if you are not liable, it will pay claims made against you by a third party. Most legal fees, settlement costs, damages to property, bodily injury and more are covered. Your general liability policy should also pay claims related to slander or libel. It will also pay for some construction-related claims as long as they fall under the completed products coverage.

Most claims not covered by the general liability coverage policy are logical. First off we can exclude every claim not related to damages that we’ve caused to others. Buildings and other property must be covered by a property form. Some liability related losses are not covered by the commercial general liability (CGL) policy. The following are some of the most obvious examples:

• Property Damage and Body Injury resulting while operating a vehicle Commercial Auto Policy

• Injuries to employees while at work Workers Compensation

• Liability coverage for Doctors, Lawyers, etc. Professional Liability

Professional liability insurance is sometimes referred to as errors and omissions insurance or E&O. Warning to the wise, take care to review all policies. Professional Liability and Errors & Omission coverages differ. While E&O is more applicable to most contractors, it’s crucial that you make sure that the product you are buying provides the coverages you need.

Why is it that certain professions need E&O insurance and other need General Liability?

First of all, I don’t think this is a simple as flipping a switch. Up for GL and down for E&O. The two are entirely different and independent coverages, and many businesses are apt to need both to be adequately insured.

We mentioned earlier that General Liability insurance doesn’t cover certain losses. We already identified a couple of the more obvious types. You should also be aware that negligence, failure to offer a service, failure to act in good faith, misrepresentation are a few additional examples of exposures not covered by a CGL policy.

Do the gaps in General Liability coverages mean that contractors and other construction-related industries need Errors and Omission coverage? Possibly, each case is different. But if you’re not considering it, then you may need to find an agent that will work through the issues and provide enough insight into the question for you to make the right decision.

Most contractors have enough exposure that they could benefit by adding E&O coverage to their existing policy. The approach TruePoint takes in exploring whether Errors and Omissions should be added is no different than the way we treat any other coverage that is required. We start defining the types of risk that are being considered. In the case of contractors E&O we would ask questions similar to those below:

1. Does your General Liability insurance protect you against claims for faulty work?

o You’re correct if you answered NO! Advance to #2.

o General Liability does not provide coverage for defective work. Call (502) 410-5089 or go to www.insuringky.com to learn more if you answered question 1 in the affirmative.

2. Does your General Liability cover your work and products?

o Again you are correct if you answered NO! Advance to #3.

o General Liability does not cover your work or products. If you answered YES visit our site www.insuringky.com to learn more about TruePoint Insurance.

Contractors can have significant gaps in coverage that can be eliminated or reduced by adding Contractors’ E&O. The next step that we advise is to determine your exposure. We begin by developing a risk profile which at a very basic level answers the following:

• your potential loss exposure (both a median or average potential loss as well as a max loss)

• the expected frequency of the type loss being considered

The final step is to help you decide if the cost of the added coverage is reasonable relative to the reduced exposure:

• We determine the cost to transfer the risk (in this case, how much will you pay for the E&O Policy)

• And we then compare the cost to insure versus the exposures identified in the risk profile.

TruePoint works with commercial accounts in Kentucky and Southern Indiana to help them better understand their business insurance needs. Our focus is on how we can help you to most effectively develop and execute a strategy for your commercial insurance needs.

I’ve heard that tragedy defines us. I disagree with that; it is how we as a group rise and address adversity that defines us. An excellent example is my grandfather’s generation. They’ve been referred to as the Greatest Generation, a fitting accolade to the group that defended our freedom and won WW II.

What is the great tragedy of our generation? Is it global warming? It could be the rise of terrorism! While I can’t answer the question, I do know that school shootings and other active shooter related incidents have to be somewhere in the mix.

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection.

The insurance industry is actively working to develop products that will protect businesses, schools and other government entities from gaps in current insurance policies. Professional liability policies were not designed to protect against active shooter risk or anything similar to that.

So what can be done and how do we do it? Products have been created and will continue to improve that will offer financial protection to entities that have been accused of failing to adequately prepare. But there is more.

Insurance companies seldom get the respect that they deserve; however, behind the scenes they are making a difference. The insurance industry is much more than a financial risk transfer vehicle, insurance companies are the leaders in making our world a safer place to leave. While most of us will never understand the significance, the insurance industry will lead America’s efforts as we deal with the risk of loss of life, mental trauma, and financial loss associated with active shooter incidents.

How? Who understands risk as well as the insurance industry? The better we understand risk exposures, the better we can prepare. The insurance industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

The insurance industry is working to make our world safer. If you are interested in learning more about the insurance industries role in managing active shooter risk you are more than welcome to contact us:

As we mentioned in part one of this discussion, a strategy for dealing with this exposure involves a significant amount of pre- and post-incident activity. Active shooter programs commonly involve the following:

Non-Insurance Services

Pre-event

Risk Assessment

Employee Crisis Training

During Event

Crisis Management

Second (Event) Responders (those who supplement initial, emergency action of fire, medical and police [first responders] and handle return services and site clean-up.)

Post-event

Counseling Services

Psychiatric Care

Public Relations Disaster Team

Investigation Assistance Funds (Rewards)

Expenses for additional, temporary security measures

Insurance Services

Liability Coverage for Lawsuits due to loss created by active shooting incident

Limits vary from $250,000/$500,000 up to multi-million dollar maximum

Business Income and Extra Expense

Limits vary from $1 million up to $100 million

Emergency medical care

Rehabilitation Expenses

Funeral and Burial Expenses

Marketing for the product targets those who are most vulnerable to this exposure such as Educational institutions, Entertainment organizations, Hotels, Healthcare providers, Religious institutions, Retail organizations, Shows (ex. Fairs, Trade Shows and Rodeos.)

Click here for Home Page

Return to Part 1

COPYRIGHT: Insurance Publishing Plus, Inc. 2018

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Headlines tragically remind us quite frequently that many aspects of our lives have become unavoidably dangerous. Sadly, this danger is due to the whim of individuals and access to weaponry. The deadly risk is the “active shooter incident.”

An active shooter incident describes a situation in which at least one person is actively killing or attempting to kill persons in a populated area. Naturally, as we are referencing a shooter, such incidents involve firearms.

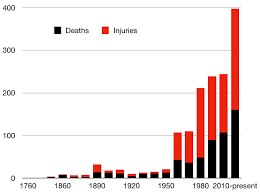

Active shootings are becoming more common. Studies made by the FBI between 2000 and 2015 indicates annual mass-shooting events rose from 6.4 per year to 20 per year. Studies also show that most shootings take place within a business or school (educational) environment. The frequency of shootings is accompanied by, on average, an increase in the number of persons killed or wounded per event.

As with any other risk that becomes significant, it is very important to find a strategy to deal with active shootings. Insurance is among the tools helpful with both pre- and post-incident planning. However, much uncertainty exists regarding protection for active shooter losses.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

Confusion may also be caused by insurance policies via the silent coverage problem. An insurance form is considered silent when it neither specifically names nor excludes a source of loss, such as shootings. It can be chaotic during the time it takes to clarify coverage gaps.

The insurance sector has a reputation as being slow to react to change. Of course, speed is never at the level that most would wish when new coverage issues arise. However, the insurance market has been stepping up and addressing the serious active shooter exposure. While there is the option of trying to amend standard policies to add protection, other ways that coverage is being addressed are separate policies that supplement insurance protection with a variety of services.

Please see part two for more information on this issue.

COPYRIGHT: Insurance Publishing Plus, Inc. 2018

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

As an investment advisor, your clients expect you to wear many different hats. Any of which would keep you busier than a three-legged cat in a sandbox:

Psychic: You’re expected to generate returns with 20/20 foresight.

Mind Reader: Investments within the tolerances of each investor’s unique goals and constraints.

Rocket Scientist: Manage risk using the qualitative and quantitative tools available to you.

When it comes to managing investments, it is critical to engage a professional. While not always obvious at first, risk management is much more than picking stocks. Failure to engage the services of a good investment advisor may be disastrous in the end.

Risk Management for Investment Advisors

As an investment manager, you are a risk manager. But risk comes in different shades. Your business is exposed to many different risks that can and should be managed. There are various paths and options to managing your business risk. But, it’s hard to envision one without the services of a specialized insurance agent.

E&O or Professional Liability coverage is one of the first risks that advisors seek to transfer. Your risk certainly doesn’t stop there, additional applicable coverages are considerable. Find the gaps in your business risk by consulting with a qualified insurance agent.

TruePoint offers a unique understanding of your industry. We understand risk management from both the advisor and insurance side. Contact us today.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection.

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection. industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.