TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

One of the biggest concerns for business owners in Pooler, GA, is the potential impact if their company cannot operate for an extended period. Without income, many businesses could face closure through no fault of their own. Fortunately, business interruption insurance can help mitigate this risk. The agents at TruePoint Insurance can guide you on how to include it as part of a new business owner’s policy (BOP) or as a standalone insurance policy.

Protection Against Income Loss

Business interruption insurance protects against income loss when your business cannot operate due to a covered peril. Common covered risks include theft, fire, wind, lightning, or falling objects. This type of insurance goes beyond covering operational expenses. Most policies provide funds for the following:

Lost revenue

Mortgage, rent, and lease payments

Loan payments

Taxes

Payroll

Relocation costs

Extra expenses for temporary rental facilities

Business Interruption Restoration Period

Your policy will specify a restoration period, which is the duration your policy will cover lost income. This period typically lasts 12 months, although some carriers may allow you to extend it for an additional fee. Policies also generally include a waiting period of 48 to 72 hours after an incident before coverage begins. Timely repairs are crucial, as delays in restoration could potentially affect your loss of income payments.

What This Policy Doesn’t Cover

Like most insurance policies, business interruption insurance has exclusions. It will not cover the following:

Broken items

Damage caused by earthquakes or floods

Undocumented income is missing from your financial records

Utilities

Shutdowns resulting from communicable diseases

Learn more about how your company can benefit from business interruption insurance. The agents at TruePoint Insurance, serving Pooler, GA, are happy to explain how this coverage works. Call our office today to get started.

Mergers and acquisitions are very complex legal transactions that, besides substantially altering regular operations, can also affect an organization’s insurance needs. Unforeseen liabilities may arise for merged entities that produce tangible products. One area of concern is a discontinued operation.

Once a product enters the marketplace, the liabilities associated with that product do not cease with the sale or merger of the original manufacturer. Such liabilities still exist even when that particular product is no longer produced. Liability claims often occur many years after the product was first produced or sold. In other words, liability still exists for operations that have been discontinued.

If the original business owner only sells its assets and retains its corporate structure, it will also retain the liabilities connected to the original operations. A business can purchase discontinued operations coverage to help in such instances. For example, Utility Trailers, Inc. built small trailers. Utility Trailers’ owners accept an attractive offer from another company and sell the business on an ‘assets only’ basis. Utility Trailers, Inc. was not dissolved as a corporate entity. A year later, some customers sue Utility, claiming loss caused by defective trailers. Their Discontinued Operations coverage will respond to the lawsuits.

Discontinued Operations coverage would provide coverage for bodily injury or property damage caused by defective products. The same coverage can be designed to provide coverage for contractors that have ceased doing business. It would be a disappointing situation to find that after a product has been discontinued or assets sold, all profit from the sale – and perhaps more – has been taken away due to a defective product that is still the responsibility of that entity. So, contact your agent and discuss whether you have continuing liability for a discontinued operation.

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Yes. If you own a business, even if it’s run out of your home, you need commercial insurance. If something were to happen to your business in Fisherville, KY, and you’re not adequately insured, you’re putting both your business and personal assets at risk. Also, you don’t want to assume that just because you work out of your home that your home-based business is covered by your home insurance policy. This is simply not true. Many homeowner’s policies severely limit the amount of coverage they provide for business-related equipment and other costs.

Millions of Americans work out of their homes. So who needs commercial insurance? Anyone who owns a home-based business like photographers, consultants, eCommerce merchants, freelancers, and more. If you work from home and you don’t work for a company, you need commercial insurance.

Commercial insurance covers the cost of any disaster that befalls your at-home office equipment. If your laptop is stolen, you can count on it being replaced. A homeowner’s insurance policy will not likely do the same. Another reason to have commercial insurance as an at-home business is the possibility of litigation. If you see clients in your home, for example, and they’re injured, you are liable. If, as a photographer, you take your clients to a nature spot and they get injured, you could be held liable. There are lots of scenarios like this one to consider.

Whether your equipment suffers theft or fire, or your face litigation, you need to be covered. Otherwise, you risk losing your business.

To learn more about purchasing a commercial insurance policy in Fisherville, KY, contact the team at TruePoint Insurance, serving this area. Our reputable agents are standing by to take your call and answer all your questions.

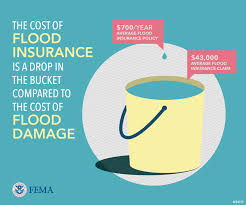

Learn about flood insurance before the waters start to rise.

Who needs flood insurance? Many residents of Georgia and South Carolina are exposed to flood risk. Those living in coastal areas are like to be more at risk. Consider the following:

River Road – It seems wise that anyone living on River Road should check in to flood insurance.

Coastal Highway – Another great clue that suggests there is a heightened risk for flooding.

Lowcountry– Since floods occur in low lying area, it’s probably wise to consider flood insurance if you live in a region known as the Lowcountry.

Anyone with Lender Requirement

Does your home mortgage require flood insurance?

Your homeowner’s policy does not protect against flooding. For anyone needing protection from rising waters, a separate Flood Insurance policy is required. This policy will provide specific coverage if your home is damaged by a local flood.

Residents in Coastal Georgia and South Carolina may find that they are required to purchase flood insurance. This requirement is most likely come for a lender. Mortgage lenders know the potential impact of floods as well as which homes are at greatest risk. Due to this risk, borrowers with homes located in a FEMA identified flood zone will likely be required to maintain flood insurance.

Needs to Cover Against Risk

Flood Loss versus Cost. You do the math!

FEMA flood zones are divided into one of many categories. These categories or buckets identified the flood risk as very risky or a Special Flood Hazard Area (SFHA). Somewhat lower-risk areas are considered Moderate Flood Hazards. There are two moderate flood hazard groups; Zone B and Zone X (Shaded). Finally, the areas that are exposed to potential flooding yet have the least risk are identified as minimal flood hazards. This grouping also has twp categories; Zone C and Zone X (Unshaded)

Even if the risk is small, you should still consider getting flood insurance. Everyone should consider buying flood insurance. This includes those without a mortgage, and those not required to have flood insurance.

When you are looking to learn more about flood insurance in Georgia or South Carolina, you should speak with the team at TruePoint Insurance. They will make work hard to make sure that your decision is as simple as possible.

One issue that may arise because of storms, extreme heat or natural catastrophe is the loss of electrical power. While power outages are often, merely a nuisance, extended power interruptions can cause problems ranging from loss of perishables (particularly frozen and refrigerated foods), damage to property that is vulnerable to temperature extremes, and personal endangerment caused by overheating or freezing.

Even if your home isn’t hit, you could go days without electricity.

Many homeowners who, for various reasons, are prone to suffering power loss, use an option to protect themselves; home generators. Such generators are capable of temporarily supplying electrical power to run household appliances and utilities. Home generators come in two basic forms:

Having a portable generator a key step in becoming storm ready!

Portable Generators – lower-powered units that operate externally from a home’s wiring system.

Standby Generators – high-power units that are attached directly to a home’s wiring system and which takes over automatically when utility power is interrupted

Regardless the type, it is critical to take proper precautions to make sure that no harm or injury results from their use.

With standby generators, installation should be performed by a licensed electrician and installations should be inspected by authorized persons before initial use. Installations should include a proper transfer switch and local utilities should be notified that an installation has occurred. Transfer switches insure that electrical power is properly and safely switched from the generator to a utility supply when power is restored.

Portable generators have a host of procedures that should be adhered to, such as the following:

generators should be located outside the home, in an area that provides proper ventilation and which shields the unit from moisture

generators should NOT be located near window or doors since carbon monoxide exhaust could seep into a home

care must be taken to prevent burns due to contact with hot generator parts

generators should never be plugged into house outlets. This can cause back feeds which results in damaging wiring and endangering utility company personnel (backed power can be transmitted through power lines at fatal power levels)

proper, exterior-rated cords should be the only kinds used with generators

generator power should be matched with essential power needs (core appliances, heating/cooling) and not overloaded (which could damage the generator and powered appliances, etc.)

fuel for generators should be stored properly and refueling should take place ONLY after the generator has cooled after being turned off

Generators can be a tremendous method to compensate for temporary power outages but care must be taken to be sure they don’t generate more problems than solutions.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

New Remote Workers are still working out the kinks

If you work from your home for part of your workweek and if the situation is an ongoing arrangement with your employer…that’s telecommuting! That is also an opportunity to make special insurance considerations. Consider the following:

Property Considerations

You may have gaps in coverage because of your work arrangement. You may not have the insurance protection you need for your employer’s business property that is kept in your home or your own property that is used to perform your job. This is because residential insurance policies severely restrict or exclude coverage for business property. A further complication is that business property usually consists of high-valued items that are vulnerable to damage and/or to theft. Such property includes fax machines, copiers, computers, pads, smart phones, computer peripherals, GPS, etc.

Liability Considerations

Personal insurance policies that include liability protection typically exclude business-related losses. Further, different policies can be quite broad in interpreting how a loss is connected to “business.” Liability Policies A and B would routinely respond to handling an insured who spilled hot coffee on a guest in his home. What if, instead of being a social guest, the visitor was your employer’s client? Policy A may still offer coverage because it considers the coffee spill to be a common home hazard. Policy B, however, may flat-out exclude the loss because the injured person was in the home for a business reason.

Vehicle Liability

Instead of using your personal vehicle for going to and from work, more of your vehicle use may be related to your job, such as making deliveries, calling on clients or visiting jobsites. Many instances of job related use might be excluded from your personal auto coverage.

Home Accidents

Simple events may be complicated when they occur in the course of performing your job at home. Coverage for injuries suffered while going up the stairs or experiencing a prolonged illness may cause coverage questions for your employer. Individual company or state-mandated coverage for employees may not apply to work-related accidents that occur at home.

Issues with working remotely

Document What You Do

In order to determine your coverage needs, you must clearly identify your exposure to business losses. Document the following:

What routine job duties do you perform in your home?

Are any tasks hazardous?

Who visits your home because of your job (clients, vendors, repair personnel, suppliers, others)? Be Specific.

How often do such persons visit?

Is a certain part of your home dedicated as a work area/office?

What equipment is used in your job? (Is the equipment used only for your job? Who owns each piece of equipment?)

Once you have a good idea of the loss exposures from performing your job at home, you need to discuss your situation with an insurance professional. An insurance pro can help you find additional coverage options as well as help to identify what coverage gaps must be addressed by your employer. While it can be liberating to telecommute, you must make sure that you haven’t given up important protection along with your cubicle or office.

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Homes may be built with solid craftsmanship and with the use of the best materials, but most residences offer little to no protection against a common hazard…..tornadoes. Recently, homeowners have begun to embrace the use of tornado shelters. Before discussing this protection method, here is some background information.

In the U.S., tornadoes most often occur in the Midwest, Plains and Southern states. Tornadoes are created by thunderstorm fronts where moist, warm air meets moving cool fronts. Winds first form a horizontal rotation that is lifted upwards by warm air. When the rotating column is tilted high enough, it becomes a tornado.

Tornadoes can occur anywhere and at any time, but the peak season is in late spring through the summer. Wind speeds range from less than 100 to +250 mph. The stronger the storm, the longer its lifespan (generally 10-15 minutes). The damage path of a hurricane is usually narrow and short, but they can be as large as a mile in width and travel tens of miles. Tornado damage can be substantial as the winds and wind-carried debris are powerful enough to demolish buildings.

When a tornado threatens a home, the safest response is to get to the lowest and innermost space; away from all doors and windows. Basements and cellars are ideal, but these features are not found in most homes. In the past, it was common to equip homes with storm cellars, located adjacent to home, to protect against severe storm winds. Today, in response to the need for more protection, there has been a revival in the use of tornado shelters.

Christie England stands in the storm shelter in front of the remains of her home May 27, 2013, in Moore, Okla. England’s home was destroyed in the May 20, 2013, EF-5 tornado that ripped through Moore. The storm killed 24, injured hundreds and damaged thousands of homes. (U.S. Air Force photo/Tech. Sgt. Bradley C. Church)

Tornado shelter are, essentially, reinforced safe rooms, ranging from regular room size, down to small enclosures that are fitted within closets or garages. They may even, like storm cellars of old, be buried in the ground. They are constructed of reinforced metal walls that are, ideally, bolted to a cement floor. Such structures are capable of staying intact even when the surrounding structure is obliterated by tornado winds. Shelters are designed to accommodate a typical family and may cost several thousand dollars.

While shelters do little to protect a residence, they do respond to the most important issue, increasing the chance that residents can survive a tornado and rebuild.

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

A variety of businesses

are routinely operated in homes. This article discusses aspects of particular

operations. Refer to Home Businesses – Basics for background information

on coverage as well as our other articles discussing different in-home

businesses.

Today’s Landlords are held responsible for their actions

Landlord

The homeowners policy is

designed to cover landlord-occupied residential buildings, landlord-owned

personal property, and loss of rents (after a fire or other covered cause of

loss), premises liability and medical payments. Note that the maximum occupancy

that may be covered under an HO policy is a four-family dwelling. A

dwelling policy may be used for 1-4 family structures that are not also

occupied by the landlord.

For landlords with

residential property containing from five to sixty units,

a Businessowners policy (BOP) is usually appropriate. It insures

buildings, landlord personal property, loss of rents (after a fire or

other covered cause of loss), premises liability and medical payments.

Most Bed and Breakfasts

do not qualify for coverage either in the homeowners or dwelling insurance

program. Bed and Breakfasts will require a combination of tenants coverage for

the resident owner/manager, and a BOP to cover buildings, landlord owned

personal property in boarders’ rooms, loss of business income (rents and fees)

and the extra expense to operate (after a fire or other covered cause of loss),

premises liability and medical payments.

Contracts often drive rental insurance policies

For landlords who have

office or retail tenants, the BOP provides broad coverages for

buildings, landlord personal property, loss of rents (after a fire or other

covered cause of loss), premises liability and medical payments.

Worker compensation is necessary for any employee. Talk with your agent. Most states require workers compensation for resident managers even if you provide only free lodging as payment. Make sure you have certificates of insurance for any subcontractors (painters, plumbers, etc.) you hire to do work for you. If the subcontractor has no insurance, you may be responsible for the subcontractor’s work-related injuries.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Homeowner (HO) policies aren’t meant to insure businesses that are run out of a home. Premiums paid for homeowner’s coverage are for handling losses related to the ownership and use of a residence and related structures. Therefore no liability coverage is available for business activities such as customers who slip and fall on your premises, damage to business property (owned or in your control), injury caused by things you make (product liability), or damage due to services that you promote or provide. It is also unlikely that an insurer would provide a legal defense against business-related claims.

Be sure to speak with your insurance agent before opening a business in your home.

Generally, an HO policy does not provide workers compensation coverage for any employee. Medical expense and liability coverage may be available for workers who are ineligible for worker’s compensation, such as maids, butlers, or nannies, but such coverage only applies if an injury occurs while performing residential tasks.

Example: You send your nanny to deliver copies of your business

proposal and, on the way to the client, she is seriously injured in a fall.

Your policy won’t provide any medical expense coverage for your nanny because

she was performing a business-related chore.

There is no coverage for detached garages, barns, or similar structures on your residence premises if they are used in whole or part for the business.

Example: You store $3,000 worth of equipment and

supplies that you use in your job in your garage and the garage burns down. The

fire loss to the garage becomes ineligible because of its partial business use.

A basic HO policy may

protect certain property. However, the coverage may be limited to as little as

a few hundred dollars. Items qualifying for limited coverage include business

personal property kept in or around your home, business personal property kept

at a location other than in or around your home or landlord’s furnishings. One

way to improve your coverage is to add policy options that do the following:

increase the coverage limits for business personal property

cover garages and other buildings that are rented to others

protect electronic business equipment which is usually used in a vehicle while such equipment is located outside of a vehicle

provide theft coverage for the landlord’s property

acquire limited business personal property and liability coverage for an in-home daycare

cover a condo unit owners’ liability for damage caused by renters

provide premises liability coverage (i.e. a customer slips and falls)

A variety of businesses

are routinely operated in homes. This article discusses aspects of particular

operations. Refer to part one for background information on coverage

basics as well as our other parts discussing different businesses.

Sales Office

Usually, an HO policy does not offer much protection for business property. In fact, available coverage may be up to only $2,500 for personal property used for business and kept on the residence premises. Further, no coverage applies to a business property such as inventory, product samples, or items being held for delivery. Finally, even optional coverage excludes property related to a business conducted on the premises. For example, you are a cosmetic sales rep who also holds make-up parties in your home. For customer convenience, you keep an inventory of cosmetics at home. The HO policy will not cover this property.

If you are a salesperson operating out of your home and have limited inventory, some companies will cover you with a Businessowners Policy (BOP). A BOP provides broad coverages for buildings, personal property, loss of business income and extra expense incurred to remain in business (after a fire or other covered cause of loss), premises liability and medical payments. If you have more than $1,000 of goods off-premises in transit, you will need to add additional coverage. Goods stored at other locations must be added to the policy.

If you cannot qualify for a BOP and a home business endorsement or separate policy fails to meet your needs, your agent will probably have to build a special commercial package policy to handle your business. Commercial lines agents have both the expertise to design the appropriate coverage and access to the markets that offer policies for your sales business.

In part one of this article, we discussed what coverage issues must be considered when running a sales office out of a home. Besides the protection previously mentioned, you will need workers compensation coverage for any employees, even part-timers, and, if you deliver anything or if your vehicle is larger than a car, van or small pickup, you may need commercial automobile insurance. Another reason for buying a commercial auto policy is if any auto is corporately owned.

Professional Offices

Regarding doctors,

attorneys, architects or similar occupations, whether your home office is your

only office or simply a satellite office, you will need to work with an

insurance agent who is familiar with the coverages that are appropriate

for professionals.

BOPs are suitable for

most professional offices and can cover buildings, personal property, loss of

business income, extra expenses incurred to operate the business (after a fire

or other covered cause of loss), premises liability and medical payments.

Consult with your agent

or your professional association(s) for professional liability and errors and

omissions coverage.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Ziplines

are a newer and wildly popular attraction. They are known by various names such

as:

zip wires

rope slides

aerial runways

flying fox

death slides

They consist of a steel

cable (or, increasingly rarely, rope), mounted at an incline between two

points. They are traversed by a person attached to the line by a harness and

pulley.

Ziplines are quite old, originally developed as a way to more easily access remote areas, such as mountain terrain, forests or as a way to cross rivers and as an aspect of climber training. They are more recently used for entertainment such at adventure camps, hiking areas in parks, amusement parks, festivals, fundraisers, in team-building exercises and, in current development, at private residences.

Safety is Critical

Ziplines are now so popular; they are sold in kit form for private use. A standard kit consists of a cable, pulley, installation kits (bolts, eyebolts, swivels, cable tensioners, turnbuckles, cable clamps, braking device, cable slings etc), handlebars, lanyards or harnesses, and other accessories. Some kits include tools such as cable grabs and cutters.

While accidents involving zip lines are low, in comparison to their use, the consequences of accidents are very high, so safe operation is incredibly important. Much of the safety has to do with ziplines being installed professionally and operated by trained personnel. The residential use of ziplines is likely to result in more accidents because of the absence of those two, critical factors.

It is important that ziplines have safety features that match the installation and use. Residential ziplines are likely to consist of short runs and be close to the ground, still it is important to make sure that there is control over the speed, that the equipment is regularly checked, that the use is properly supervised, that there is proper clearance so that hands, clothing or hair don’t become entangled and that the launch and stopping points are properly supported. Items that help make zipline use safer is the use of a shock-absorbing landing zone, backup lanyards or harnesses, goggles, thick leather gloves (for emergency braking), helmets, masks, and knee pads.

Of course, it is

supremely important that the zipline use the right

type of cable, have a proper incline, be properly

tensioned and that the right attachment and anchor points are used and that the

space for the installation is adequate. The installation site must be

absolutely free of obstacles, so site preparation is often necessary.

Maintenance is very important, particularly with regard to line wear and

tension and zipline owners must inspect their

installation and gear carefully and regularly. Safe procedures and supervision

is also critical.

You may also find it

helpful to see our article titled, “Who Cares about Attractive Nuisances” for

related information.

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All rights reserved. Production or distribution, whether in whole

or in part, in any form of media or language; and no matter what country, state

or territory, is expressly forbidden without written consent of Insurance

Publishing Plus, Inc.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions