TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

Damaged Chimneys Significantly Increase the Risk of Home Fires

Chimneys often enhance a home’s roofline as well as add a decorative interior feature (fireplace) to a home’s interior. However, it is the chimney’s function that deserves the most attention. They are intended to safely disperse the heat and smoke that result from the use of a fireplace. Fireplace fires reach very high temperatures that take their toll on chimneys. It is risky to regularly use fireplaces without making sure that the chimney is in a safe condition.

An April 2015 report from the U.S. Consumer Product Safety Commission reveals that, on average, more than 20,000 fires occur annually across the U.S. that are directly related to chimneys and chimney connections (found with wood-burning stoves and fireplace inserts).

One particular danger

when buying an existing home that has a fireplace is that the chimney may have

experienced a previous fire. There are certain signs to look for that are red

flags, such as the following:

Unsafe Chimneys: Know the Signs

Chimney flue tiles are missing or damaged

Creosote (tar colored) flakes appear on roof or ground adjacent to the chimney

Creosote that looks puffed or bubbled

Chimney damper appears warped

Exterior masonry has smoke-darkened cracks

Rain cap appears darkened from smoke and/or has a distorted shape

Roofing near chimney appears heat or smoke damaged

Chimney fires can be

hidden, intense and even explosive, typically causing very serious levels of

damage, often life-threatening. If you make use of a fireplace, wood-burning

stove or an insert, it is very important to get them regularly and

professionally inspected.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole

or in part, in any form of media or language; and no matter what country, state

or territory, is expressly forbidden without written consent of Insurance

Publishing Plus, Inc.

The real estate market continues to be very strong due to the local economy and new developments opening up all over the place. When you are looking to buy real estate in Fisherville, getting a condo could be a great option. If you do buy a condo, you need to make sure that you have it properly covered by a full condo insurance policy. There are several things that a Fisherville, KY resident needs to know about condo insurance.

Valuable Coverage

Most importantly, you need to remember that you get very valuable coverage from condo insurance. This will include coverage in the event your property is damaged or destroyed and will also include liability coverage. In the event of an accident or unfortunate situation, this could prove to be very helpful for you. A home associations policy will not cover your property.

Likely Requirement

Another factor to remember is that you will likely be required to carry the condo insurance policy at all times. If you took out a loan to buy the condo, your lender will likely want you to have condo insurance to make sure that their collateral is protected. Even if you don’t have a mortgage the condo association will likely require that you have coverage. This ensures that you have liability coverage in the event you cause damage to another condo or the common areas.

Your Kentucky condo is a major asset that you need to properly cover by insurance. When you are trying to cover your condo with insurance, you should reach out to TruePoint Insurance in Fisherville, KY to start the process. The insurance professionals at TruePoint Insurance can help you to better assess your individual risks. We will then help you find a condo policy that will properly cover you and your condo.

Haunted houses have been a part of Halloween in America for

over 75 years. Many of the first haunted houses were associated with

corporations. Yet, it was the nonprofit sector that made haunted houses a part

of Americana.

In recent year’s haunted houses started to fade. Sponsoring organizations such as churches, and school groups, have backed away. Like so many other things in our lives, the culprit is government red tape.

Personal Injury Claims and Haunted Houses

Haunted House

In the past, successful lawsuits against haunted houses have

been limited. We can point to three factors that significantly contributed to

this:

Consumers can readily identify and assume the risk

Haunted houses are open for only a brief time each

year. The risk of something going wrong

increases with time. Since these events

are seasonal dangerous conditions are less likely to develop.

Proof! Claims of

injury or damages were often dismissed due to lack of proof. What’s changed? Cell phones!

Access to information relative to compensation for injuries or damages.

It’s not the haunted house; it’s the Attorneys that scare me!

That was the past. If someone is injured at a Special Event today, they are much more likely to seek compensation. Recently I did an online search for “Haunted Houses.” I should have known better. But the truth is, what I found was horrifying. On page one of my search results was a blog post from a personal injury attorney.

Times have changed.

Seasonal Events have become considerably riskier. If you are planning a haunted house,

hayride, or any other seasonal event, take a moment an to consider the

risk. It’s also wise to reach out to an

independent insurance agent for input. Most agents will likely recommend

insurance if appropriate. They may also provide insights into your

process. Identifying opportunities to

reduce or avoid risk. They should also

present products to transfer risks associated with production. Some of the more

common suggestions are:

Waiver or Release

Before allowing entry most all require a signed release or

waiver of liability. As long as the

disclosures describe the risk, consumers to sign the waiver assume the risk.

Limited Liability Company (LLC) or Incorporate (Inc.)

Setting up a business entity is an excellent way to limit

liability. Undertakings done with these corporate structures are separate from

your personal assets.

General Liability Insurance

General Liability Insurance protects a business against

bodily injury or property damage claims. Tripping over a cord, cuts caused by

exposed nails, injuries or losses caused by chemicals, and falling props: are a

few examples where GL coverage would provide protection.

Workers Compensation Insurance

Work Comp protects employees that become injured while

working for you. If your special event has employees, you need this coverage.

There are very few exceptions to this. Special rules apply to partners,

sub-contractors, members, and volunteers. Call an Independent Insurance Agent

for a better understanding of your requirements.

Property Insurance

Your Special Event may alter coverage needs on buildings

that you own or lease. It is essential to discuss your event with your

insurance agent.

Inland Marine

You may use mobile equipment or other property in your

haunted house or corn maze. This should

be covered with inland marine coverage.

Commercial Auto

Most automobiles used in your Special Event will already

have coverage. The question is, will they have enough? Unless your vehicles are

owned by an LLC or other business, then your entity is exposed. It needs to be!

In the event of legal action, your organization most likely will be named in

any lawsuits. To protect yourself from this, you should consider Hired and Non-Owned

Coverage.

Volunteer Accident Insurance

Injuries to employees are covered by the work comp policy. But what happens if a volunteer is injured? They can most likely be covered by purchasing a Volunteer Accident Policy. However, there are many gray areas where you might run aground. We suggest that you speak with an independent Insurance Agent beforehand.

Fall is the season for haunted houses, corn mazes, and other

seasonal events. Common sense, caution, and communicate with a commercial

insurance agent. It’s the best approach

if your planning to host any of these.

Call a TruePoint Insurance Commercial Agent at (502)

410-5089. They will be happy to discuss your options in managing your specific

risk.

Mobile homes are vulnerable to serious damage from winds and storms since they are smaller and much lighter than stick-built or factory-built homes. It is important to use reinforcements to make them more stable; such as tie-downs.

Tiedowns come in two basic types; over-the-top tie-downs and frame anchors. Over-the-top tie-downs are straps that resist lifting forces and minimize tip-overs. They are usually used with single-wide mobile homes. Strapping is placed with over the top of the roof or over the structure’s sides. Frame anchors are reinforcements that resist lateral forces, making a structureless vulnerable to sliding off supports

In order to stabilize a structure, the tie-downs must be properly anchored to a foundation, slab or the ground. Anchor types include the following:

Tying down Mobile Homes

·

Hard Rock Anchor

·

Concrete Slab Anchor

·

Cross Drive Rock

Anchor

·

Drive or Barb Anchor

·

Auger Anchor

·

Disc Anchors

Straps and anchors have to be used properly and they have to meet various standards such as placement of anchors, anchor fittings, method of installation and ground/site conditions. When anchored to the ground, it may be necessary to make test its suitability as an anchor. If piers and footings are used they must be able to meet various requirements regarding weight support, dimensions, material quality, pier placement, and other areas. Straps and anchors also have to meet requirements in order to be depended on to withstand the stresses winds and other forces.

Use of tie-downs varies by state, state regulations and soil type. Local building inspectors and mobile and manufactured home builder associations are excellent sources for anchoring and tiedown requirement information. Use of that valuable information, along with insurance, is great methods for fully protecting a mobile home.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution,

whether in whole or in part, in any form of media or language; and no matter

what country, state or territory, is expressly forbidden without written consent

of Insurance Publishing Plus, Inc.

Ziplines

are a newer and wildly popular attraction. They are known by various names such

as:

zip wires

rope slides

aerial runways

flying fox

death slides

They consist of a steel

cable (or, increasingly rarely, rope), mounted at an incline between two

points. They are traversed by a person attached to the line by a harness and

pulley.

Ziplines are quite old, originally developed as a way to more easily access remote areas, such as mountain terrain, forests or as a way to cross rivers and as an aspect of climber training. They are more recently used for entertainment such at adventure camps, hiking areas in parks, amusement parks, festivals, fundraisers, in team-building exercises and, in current development, at private residences.

Safety is Critical

Ziplines are now so popular; they are sold in kit form for private use. A standard kit consists of a cable, pulley, installation kits (bolts, eyebolts, swivels, cable tensioners, turnbuckles, cable clamps, braking device, cable slings etc), handlebars, lanyards or harnesses, and other accessories. Some kits include tools such as cable grabs and cutters.

While accidents involving zip lines are low, in comparison to their use, the consequences of accidents are very high, so safe operation is incredibly important. Much of the safety has to do with ziplines being installed professionally and operated by trained personnel. The residential use of ziplines is likely to result in more accidents because of the absence of those two, critical factors.

It is important that ziplines have safety features that match the installation and use. Residential ziplines are likely to consist of short runs and be close to the ground, still it is important to make sure that there is control over the speed, that the equipment is regularly checked, that the use is properly supervised, that there is proper clearance so that hands, clothing or hair don’t become entangled and that the launch and stopping points are properly supported. Items that help make zipline use safer is the use of a shock-absorbing landing zone, backup lanyards or harnesses, goggles, thick leather gloves (for emergency braking), helmets, masks, and knee pads.

Of course, it is

supremely important that the zipline use the right

type of cable, have a proper incline, be properly

tensioned and that the right attachment and anchor points are used and that the

space for the installation is adequate. The installation site must be

absolutely free of obstacles, so site preparation is often necessary.

Maintenance is very important, particularly with regard to line wear and

tension and zipline owners must inspect their

installation and gear carefully and regularly. Safe procedures and supervision

is also critical.

You may also find it

helpful to see our article titled, “Who Cares about Attractive Nuisances” for

related information.

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All rights reserved. Production or distribution, whether in whole

or in part, in any form of media or language; and no matter what country, state

or territory, is expressly forbidden without written consent of Insurance

Publishing Plus, Inc.

Kentucky is one of the most expensive states for auto insurance.

If you live in Kentucky and own a car, then you’re paying too much for Automobile Insurance.

If someone is telling you otherwise, I’ve got some excellent advice for you. Stop listening to that person! They obviously don’t have a clue about the cost of auto insurance in Kentucky.

.

Proving that the cost of Kentucky Auto Insurance is High

The Proof

Which states would you expect to pay the most for insurance? States with bigger cities, and heavy traffic? Commonsense would lead most of us to expect to find New York, California, and New Jersey at the top of the list. Using the same logic we can also add Massachusetts, Illinois, Florida, and Connecticut. And while not a state, I would also expect to see Washington D.C. on a list of states with higher auto insurance premiums.

Six states have average auto

insurance rates that range from $1,750 to $2,500. Starting with the most expense:

1. Michigan

2. Louisiana

3. Florida

4. Connecticut and,

5. New York

6. Kentucky

For the most, this likely seems appropriate. But for many it will be eye-opening to find how high car insurance is in the Commonwealth of Kentucky. Surprisingly the residents of Kentucky pay more for auto coverage than California. The same is true for Washington D.C., Maryland, New Jersey, Massachusetts, and Illinois.

Who is this person that says you’re

car insurance is not expensive?

Kentuckians on average spend $1,752 annually for auto insurance. That’s almost 30% more than the national average. It is a fact; your auto insurance is expensive.

If you are a good driver in Kentucky, you pay too much for insurance.

If you’re a bad driver you pay too much.

Kentucky car owner’s that drive too fast, pay to much.

Compared with most other states, Kentucky auto insurance cost more. While this is true for most residents, not everyone in Kentucky overpays. Uninsured and underinsured drivers clearly don’t pay too much for car insurance. But don’t read that to say that this group doesn’t have a hand in cost of car insurance in Kentucky. Their contribution is significant. Those that drive with inadequate auto coverage, raise auto premiums for everyone. This increase in state demand for uninsured and underinsured motorist coverage. Which in turn places upward pressure on the overall cost of auto insurance premiums.

It’s a fact that Auto Insurance is higher in Kentucky than it is in most states

The price for car insurance in

Kentucky is high. Some may try to argue

this. Beware of those that argue against

the facts.

Kentuckian plays about $400 a year more than the U.S. Average. Why is Kentucky auto insurance so

expensive?

How does Kentucky compare to other states in our region? To the north, Kentucky borders, Illinois, Indiana, and Ohio. Each of these states is ranked as one of the ten least expensive U.S. States for car insurance. The average auto premium for the three is $973. Compared to these three Mid-Western states, Kentuckians are paying almost $800 a year.

Why are we still listening to the nuts that still think we aren’t paying too much to insure our personal auto?

If you would like to have an insurance agent look you in the eye and tell you:

“Yes, you are paying too much to insure your

car,” then try TruePoint.

Want to learn about factors that make Kentucky auto insurance the 6th highest in the U.S.?

Give us a call at (502) 410-5089.

Serious about lowering your auto insurance cost? Then get your insurance documents together.

Call or drop by, and we will do our best to help you reduce the value of your home and auto insurance.

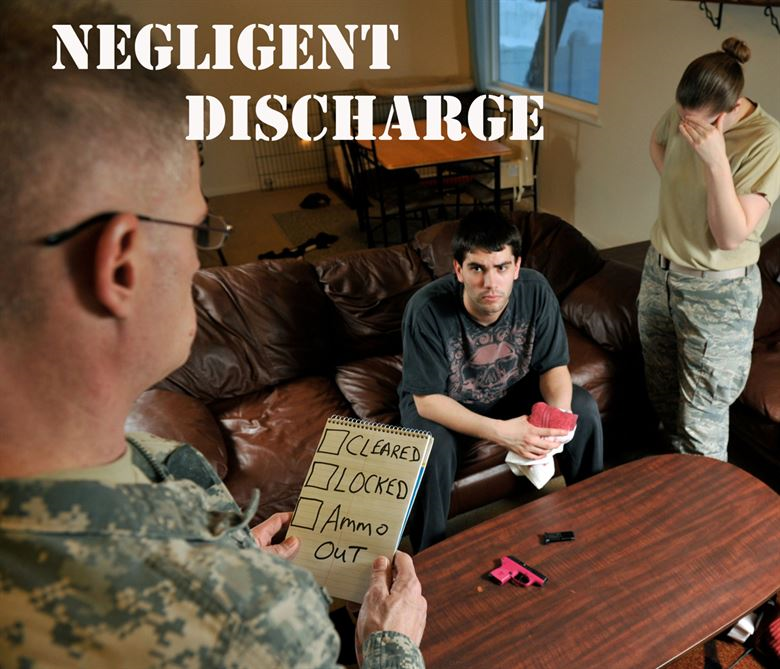

In 2010,

during a party that involved minors drinking alcohol, one guest was shot and

killed when a gun, being played with by its owner (another party attendee) went

off. The parents of the deceased sued the parents of the gun handler. The

latter requested coverage from their homeowner insurance company. The company

denied coverage and, eventually, a court ruled that no obligation existed under

the insurance policy. The company was released from the lawsuit.

Homeowners coverage, like other insurance policies, is

intended to protect against losses that are accidental. Often, accidental

losses can be readily determined, but incidents involving firearms are

complicated.

Accidental discharge of a gun can be a crime

When one

person injures another, both the act and the intent are considerations of

whether an incident is an accident. In the shooting incident mentioned above,

it was determined that the gun handler was guilty of negligently handling the

gun and was jailed. Since a court determined the incident was a crime, it did

not qualify as an accident. A loss caused by a crime is ineligible for

coverage.

When a

loss involves firearms, it is often treated far differently than other

circumstances. Consider the following:

Jim is

hosting a party at his house for a bunch of high school friends and Fran is one

of the persons attending it. Jim, well known to his friends as the group’s

clown, is fooling around with an item. Fran, who is nearby, is seriously

injured. Later, Fran’s family sues Jim’s parents and they file the lawsuit with

their insurance company.

Scenario

one – Jim recently became interested in tennis. He brings out a very expensive

tennis racket he just received. He brags about how light and powerful it is and

he demonstrates strokes. When he demonstrates a backhand, Fran is passing

behind him and she is hit, suffering a broken nose and several shattered teeth!

Scenario

two – Jim recently became interested in firearms. He brings out a very

expensive pistol he just received. He brags about how light and powerful it is

and he demonstrates how it is supposed to be handled. When he demonstrates how

to aim it, the gun fires and Fran is struck. The bullet hits and fractures her

shoulder.

In both

scenarios, the injuries are a result of Jim’s immature and careless action. In

both situations, no harm was intended. In both instances, Fran is seriously

injured. In all likelihood, the losses will not be handled similarly. A tennis

racket is a piece of equipment that is intended to be used for a particular

sport. It is used for hitting tennis balls and other uses are considered

unusual and, for the most part, not dangerous. This loss has a very high chance

of being treated as an accident.

A gun is

a weapon. It is used for both defensive and offensive purposes and, by nature,

is capable of extremely serious, often deadly harm. It is considered to be a

dangerous instrument. Therefore, the stakes are far higher whenever a gun or

other firearm causes a loss. In many instances, even when harming another party

is completely unintended, acts involving firearms also involve far more

accountability and may not be classified as accidental. In the shooting

scenario, the chance is very high that the loss would be denied.

Because of the danger inherent in guns, it’s important to be aware that losses involving them are often ineligible for insurance protection. That makes it critical that their ownership is treated seriously and every possible precaution against unintended injury be taken.

COPYRIGHT: Insurance Publishing Plus, Inc., 2016

All rights reserved. Production or distribution, whether in whole

or in part, in any form of media or language; and no matter what country, state

or territory, is expressly forbidden without written consent of Insurance

Publishing Plus, Inc.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions