Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

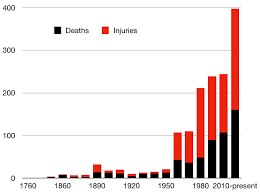

Get DirectionsAs we mentioned in part one of this discussion, a strategy for dealing with this exposure involves a significant amount of pre- and post-incident activity. Active shooter programs commonly involve the following:

Non-Insurance Services

Pre-event

Risk Assessment

Employee Crisis Training

During Event

Crisis Management

Second (Event) Responders (those who supplement initial, emergency action of fire, medical and police [first responders] and handle return services and site clean-up.)

Post-event

Counseling Services

Psychiatric Care

Public Relations Disaster Team

Investigation Assistance Funds (Rewards)

Expenses for additional, temporary security measures

Insurance Services

Liability Coverage for Lawsuits due to loss created by active shooting incident

Limits vary from $250,000/$500,000 up to multi-million dollar maximum

Business Income and Extra Expense

Limits vary from $1 million up to $100 million

Emergency medical care

Rehabilitation Expenses

Funeral and Burial Expenses

Marketing for the product targets those who are most vulnerable to this exposure such as Educational institutions, Entertainment organizations, Hotels, Healthcare providers, Religious institutions, Retail organizations, Shows (ex. Fairs, Trade Shows and Rodeos.)

Return to Part 1

COPYRIGHT: Insurance Publishing Plus, Inc. 2018 All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

RVs mean time spent with family and friends on the open road. They represent adventures and the opportunity to develop lasting memories of time together. Just as you are required to insure your regular vehicle, you are also required by law to carry insurance on your RV. The situation that an RV represents is different than a normal vehicle and your insurance needs will also be different as well. Consider this; an RV is both a vehicle and a vacation home. When you are looking at various insurance options, it’s important to consider the pitfalls that you could encounter while you are away from home. The team at TruePoint Insurance serves the needs of Kentucky, Indiana, and Tennessee residents. They understand the

RVs mean time spent with family and friends on the open road. They represent adventures and the opportunity to develop lasting memories of time together. Just as you are required to insure your regular vehicle, you are also required by law to carry insurance on your RV. The situation that an RV represents is different than a normal vehicle and your insurance needs will also be different as well. Consider this; an RV is both a vehicle and a vacation home. When you are looking at various insurance options, it’s important to consider the pitfalls that you could encounter while you are away from home. The team at TruePoint Insurance serves the needs of Kentucky, Indiana, and Tennessee residents. They understand the  Ok, that’s a bit of a stretch. I pretty sure your insurance will not cover you that far away from home. So how far can you go and still have RV Insurance coverage?

Ok, that’s a bit of a stretch. I pretty sure your insurance will not cover you that far away from home. So how far can you go and still have RV Insurance coverage?

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security. Business owners have a lot at stake when it comes to determining whether persons connected with their ventures are employees or independent contractors. The largest issue with making this determination involves taxes and insurance.

Business owners have a lot at stake when it comes to determining whether persons connected with their ventures are employees or independent contractors. The largest issue with making this determination involves taxes and insurance.

Because of the position held by policyholder/insureds and insurance companies, the classification of workers is often in conflict as insureds desire liberal coverage and insurers wish to restrict protection to qualified persons. However, both parties are best served when worker classifications are clear. Premiums charged to policyholders are based on correctly recognizing the parties eligible for coverage. Proper classification keeps coverage affordable and makes the insurance process more efficient. Coverage involving employees should be connected to an applicable business that employs them. Coverage involving independent contractors should be connected to the contractors. In other words, they should secure their own, separate coverage.

Because of the position held by policyholder/insureds and insurance companies, the classification of workers is often in conflict as insureds desire liberal coverage and insurers wish to restrict protection to qualified persons. However, both parties are best served when worker classifications are clear. Premiums charged to policyholders are based on correctly recognizing the parties eligible for coverage. Proper classification keeps coverage affordable and makes the insurance process more efficient. Coverage involving employees should be connected to an applicable business that employs them. Coverage involving independent contractors should be connected to the contractors. In other words, they should secure their own, separate coverage. Insurers commonly provide coverage for mobile/manufactured homes by modifying a conventional homeowner policy with provisions called endorsements. The endorsements change key definitions and other elements of a conventional policy to fit a mobile or manufactured home situation. The result is a modified homeowner package that protects the home, outbuildings (unattached garages, sheds, etc.) and personal property. They also provide insurance for personal liability. Regardless of the type of home you own or live in,

Insurers commonly provide coverage for mobile/manufactured homes by modifying a conventional homeowner policy with provisions called endorsements. The endorsements change key definitions and other elements of a conventional policy to fit a mobile or manufactured home situation. The result is a modified homeowner package that protects the home, outbuildings (unattached garages, sheds, etc.) and personal property. They also provide insurance for personal liability. Regardless of the type of home you own or live in,  Any coverage option you choose is likely to reflect the fact that mobile homes are, well, mobile. Therefore coverage is affected by the fact that mobile homes:

Any coverage option you choose is likely to reflect the fact that mobile homes are, well, mobile. Therefore coverage is affected by the fact that mobile homes:

and homes. Essentially insurance is offered on a package basis, meaning that there is coverage for physical property as well as protection against the legal and financial consequences of injuring others or damaging property that belongs to others.

and homes. Essentially insurance is offered on a package basis, meaning that there is coverage for physical property as well as protection against the legal and financial consequences of injuring others or damaging property that belongs to others.

For most of us, our relationship with aviation is passive. We, except for rare instances, are involved in flight as passengers, not as flight crew. We board aircraft, take our seats and allow pilots to transport us, handling all of the complexities of air travel.

For most of us, our relationship with aviation is passive. We, except for rare instances, are involved in flight as passengers, not as flight crew. We board aircraft, take our seats and allow pilots to transport us, handling all of the complexities of air travel. frequency but high severity accidents. Currently such policies are now being asked to handling an emerging, different exposure; unmanned aerial vehicles (UAVs).

frequency but high severity accidents. Currently such policies are now being asked to handling an emerging, different exposure; unmanned aerial vehicles (UAVs).