Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get DirectionsAre you a homeowner in the beautiful Savannah, GA area? If so, it’s time to get to know your neighbors at TruePoint Insurance. We are proud to help area residents with all of their insurance needs. Give us a call, or stop by our office today to find out how we can help you protect your home.

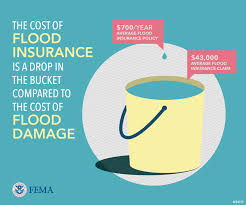

Do you have the right insurance policy protecting your home?

Protecting your home with the right insurance policy is a large part of responsible homeownership. You may not overthink your various insurance policies, but you’ll be happy to have them if you experience a significant loss! Because of this, it’s vital that you have the right policy in place with the appropriate level of protection.

If it’s been a while since you’ve thought about your policy or given it a careful review, there’s no time like the present! Putting forth the effort to ensure that you have the right policy in place can save you a lot of headaches down the road. Home insurance serves many purposes, and giving it a regular review isn’t a bad idea at all.

Your home insurance policy is the first step in ensuring that your family home is protected now and well into the future. Making sure that you have the right policy for your needs is something your local agent can help you with.

Let us help you with all of your insurance needs!

Savannah, GA area residents can rely on TruePoint Insurance for help with their home insurance needs. Now’s a great time to find out if you have the right insurance policy for your home. If you want to find out more, give us a call or stop by today!