TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

This is a term originated by a judge to describe a property that attracts youngsters and, because of its dangerous nature, creates a special obligation to property owners. Examples are:

swimming pools

trampolines

empty buildings

appliances kept outside

excavations

construction materials

zip lines

All of these can lure children onto

property and they all have the potential to cause serious injury.

Why Do Attractive Nuisances Create

A Special Obligation?

A special obligation exists because

of such property’s child endangering nature. Children do not have the reasoning

ability of adults. When an opportunity to have fun pops up, it’s a rare child

who thinks about the chance of being injured. A property owner with an

attractive nuisance on his property cannot escape liability because of a

trespassing child. When an attractive nuisance is involved, adults have to make

a special effort to protect children from their blind sense of adventure or face

the consequences.

How Do You Handle Attractive

Nuisances?

Pool Safety starts with controlling access.

The answer is…doing whatever it

takes to prevent a child’s access to the nuisance. Therefore, in order of their

effectiveness:

1. Eliminate the nuisance

have old appliances hauled to a junkyard

tow old, non-running vehicles away

get rid of construction materials immediately after a building project is complete

2. Secure the nuisance

take off doors or covers from large appliances awaiting garbage

pickup

keep sharp tools, especially power tools and equipment, locked

away

store construction materials in a garage or shed

3. Reduce the chance for injury

from a nuisance

install a pool cover and have a locked fence to prevent access to the pool

do not allow younger children to use equipment such as trampolines

make sure there’s adult supervision of children using play equipment

If you’re not certain about whether

you have an attractive nuisance situation, discuss the situation with an

insurance professional.

COPYRIGHT:

Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without the written consent of Insurance Publishing Plus, Inc.

A standard homeowner’s policy offers a limit equal to half of the amount reserved for the residence to protect against loss to a given residence’s personal Property (ex. Your home is covered for $150,000, so your contents and furnishings are covered for $75,000). While this is generous coverage, it doesn’t extend to all types of the property nor for all causes of loss. Certain types of property, because of its high value and liquidity, is far more vulnerable to loss…either easily destroyed, easily stolen or both. So, to compensate for this difference, insurers use coverage restrictions.

Property claims due to theft are subject to lower limits

Theft Coverage Limitations

When property is lost due to theft, coverage under a standard

homeowner policy is severely limited (generally $1,000 – $2,500) for the

following types of property:

jewelry, watches, furs, and gemstones

dinnerware, serving sets, trophies and similar property

made of or plated with silver, gold, platinum or pewter

for firearms, accessories and related property

Other Coverage Limitations

Several categories of

property are subject to very modest limits ($200 – $2,500) of coverage,

regardless of the cause of loss (theft, fire, accidental breakage, etc.).

Specifically:

money, banknotes, coins, medals, gold, silver, and platinum (other than jewelry or dinnerware)

securities, accounts, deeds, tickets, stamps, manuscripts, passports and similar property

watercraft and related property including their trailers

trailers not used with watercraft

business property located in your residence

business property located away from your residence

certain types of electronic property which are lost or damaged while in a car or is located away from your home and used for business.

Handling the Limited Coverage Situation

Insurance companies are happy to provide more coverage if they are paid for their trouble. Specifically, limited coverage can be handled using the following methods:

Increased Coverage C Endorsement – this form is only appropriate for

property saddled with limited coverage for theft losses. This form is attached to

a basic policy and it increases the theft insurance limit (i.e. for jewelry

from $1,500 to $5,000).

Scheduled Personal Property Endorsement – this form is used for increasing

coverage for property that has protection reduced for all sources of loss. The

property is removed from the basic policy’s limits and is covered exclusively

by the endorsement. This form takes more work since each item of property has

to be listed and assigned a particular insurance limit.

Inland Marine Property Floater – this method works like the personal

property endorsement, except that it is a separate policy. This alternative is

more appropriate for persons owning substantial amounts of high-valued

property. The coverage must often be purchased from specialized insurers and comes

at a high cost. In order to qualify for such coverage, you may need to meet

special circumstances such as having a residential alarm system or make use of

vault storage.

Another Advantage of Special Handling

In order to arrange coverage under a schedule or an inland marine policy, the property must be properly valued. This often involves appraising the property. It’s very helpful to have an expert source to establish the current value of jewelry, furs or other valuable possessions. In fact, such property should be appraised every two or three years since their values often increase over time.

Do you still have questions about property that needs special

handling? Talk to an insurance professional about your needs and make sure that

you have proper protection.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution,

whether in whole or in part, in any form of media or language; and no matter

what country, state or territory, is expressly forbidden without written

consent of Insurance Publishing Plus, Inc.

Each day more people decide to create their own Websites, blogs or otherwise participate in social media activities. The reasons for having a Website or blog vary or other activities range from frivolity to earnestness. Personal Websites and blogs commonly describe the host, his or her family, and interests such as a particular hobby, sports, profession, humor, etc. Whatever the reason for creating a Website or blog, they, along with social network activity can represent an additional source of loss that may require additional insurance. The loss potential is directly related to the purpose and content found on the Website.

New Opportunity For Old Losses

Website liability is an extension of the age-old accountability for what you say or write. Such responsibility extends to household members; so it’s important to be aware of what a family’s little E-wizard may be doing. The types of losses that may be created by a Website, blog, or social media activity include:

Libel – knowingly publishing false information that harms a person’s reputation.

Invasion of Privacy – disclosing information that interferes with another party’s peace of mind.

Infringement – violating or interfering with another’s property rights or the right to pursue business

Oops, You May Not Be Covered

Are you insured for libel and slander? Most aren’t!

Most homeowner policies protect against liability for tangible injury to another person or for actual damage to another party’s property. Liability created by publishing or broadcasting content typically involves a personal (or non-physical) injury that is not covered by a typical homeowner policy. While individuals may be able to add protection (such as add-ons to a homeowner policy or umbrella coverage), certain losses may still be uncovered because they involve intended acts or business activity.

Can You Protect Yourself?

The good

news is you can take steps to eliminate or, at least, minimize the possibility

of facing electronic publishing-related loss. The first step is to identify

areas of concern. The key to understanding and addressing any possible Website

liability is to focus upon:

the nature of

the Website or activity

the Website or

account’s contents

who may be

harmed by the site or activity

how a party may

be harmed

It is

important that you think hard about these issues and approach the job

objectively. Your building a site, blogging or using social media

just for “fun” could end with you explaining the punch line in court.

Two people can interpret information in radically different ways. Use a method

of examining your Website that helps you view it through “fresh” eyes

that won’t gloss over important facts. Asking the help of others could be a big

plus.

Considerations

For Your Web Site, Blog or Social Networking

If you or

someone in your household operates or is building a Website, or is active with

social media, you need to be aware that the site (or activity) could open you

to legal situations. Here are some questions you should consider:

Who

created the site or page?

Key

consideration: depending upon the circumstances, a private party that created

the site for you may share (or even own) the responsibility for damages caused

by the site.

What is

the purpose of your site or activity?

Key

consideration: Is there ANY business activity or purpose? If so, you may have

an immediate need to secure appropriate protection.

What

content is found at your site or page?

Key

consideration: Not only do you have to think about YOUR message, but you must

think of other parties that appear at your site such as friends, companion

businesses or even miscellaneous links.

Who do

you intend to attract to the site and how do visitors use your page?

Key

consideration: There’s a big difference in the type of people you’re targeting,

such as inviting:

relatives to see

baby pictures or family newsletters

customers to

request product/service information or to place orders

hobbyists to

distribute or solicit stories or advice

strangers to a

forum for discussing sports, political or other topics

Is there

anyone you would not want to see the site or page? Why?

Key consideration:

Answering this question honestly is critical. It can identify prime sources for

possible legal action against you. It may also suggest what precautions you may

take, including the easiest action such as eliminating the reference to a

person, group or organization.

Does Your

Site or Activity Create An Insurance Need?

After

examining the key concerns about your Website, you should be prepared to take

precautions which may include:

adding security

features to your Website

changing the

content

adding waivers

or disclaimers about links or certain pages that appear on your site

adding user agreements

to your site

creating

guidelines on maintaining current and future content at the site

changing your

homeowner coverage

buying

additional or special personal or business liability insurance

adding or

eliminating a guest book (if you have a guest book, pay close attention to

what visitors say)

eliminating the

Website

Once

you’ve carefully examined your situation, a discussion with an insurance

professional could be an excellent step to identify coverage needs which may

include having to buy commercial coverage. The instant and widespread access

represented by the Internet creates new perils for individuals. Don’t hesitate

to seek the help of an insurance professional or even competent legal advice.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without the written consent of Insurance Publishing Plus, Inc.

Damaged Chimneys Significantly Increase the Risk of Home Fires

Chimneys often enhance a home’s roofline as well as add a decorative interior feature (fireplace) to a home’s interior. However, it is the chimney’s function that deserves the most attention. They are intended to safely disperse the heat and smoke that result from the use of a fireplace. Fireplace fires reach very high temperatures that take their toll on chimneys. It is risky to regularly use fireplaces without making sure that the chimney is in a safe condition.

An April 2015 report from the U.S. Consumer Product Safety Commission reveals that, on average, more than 20,000 fires occur annually across the U.S. that are directly related to chimneys and chimney connections (found with wood-burning stoves and fireplace inserts).

One particular danger

when buying an existing home that has a fireplace is that the chimney may have

experienced a previous fire. There are certain signs to look for that are red

flags, such as the following:

Unsafe Chimneys: Know the Signs

Chimney flue tiles are missing or damaged

Creosote (tar colored) flakes appear on roof or ground adjacent to the chimney

Creosote that looks puffed or bubbled

Chimney damper appears warped

Exterior masonry has smoke-darkened cracks

Rain cap appears darkened from smoke and/or has a distorted shape

Roofing near chimney appears heat or smoke damaged

Chimney fires can be

hidden, intense and even explosive, typically causing very serious levels of

damage, often life-threatening. If you make use of a fireplace, wood-burning

stove or an insert, it is very important to get them regularly and

professionally inspected.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole

or in part, in any form of media or language; and no matter what country, state

or territory, is expressly forbidden without written consent of Insurance

Publishing Plus, Inc.

Mobile homes are vulnerable to serious damage from winds and storms since they are smaller and much lighter than stick-built or factory-built homes. It is important to use reinforcements to make them more stable; such as tie-downs.

Tiedowns come in two basic types; over-the-top tie-downs and frame anchors. Over-the-top tie-downs are straps that resist lifting forces and minimize tip-overs. They are usually used with single-wide mobile homes. Strapping is placed with over the top of the roof or over the structure’s sides. Frame anchors are reinforcements that resist lateral forces, making a structureless vulnerable to sliding off supports

In order to stabilize a structure, the tie-downs must be properly anchored to a foundation, slab or the ground. Anchor types include the following:

Tying down Mobile Homes

·

Hard Rock Anchor

·

Concrete Slab Anchor

·

Cross Drive Rock

Anchor

·

Drive or Barb Anchor

·

Auger Anchor

·

Disc Anchors

Straps and anchors have to be used properly and they have to meet various standards such as placement of anchors, anchor fittings, method of installation and ground/site conditions. When anchored to the ground, it may be necessary to make test its suitability as an anchor. If piers and footings are used they must be able to meet various requirements regarding weight support, dimensions, material quality, pier placement, and other areas. Straps and anchors also have to meet requirements in order to be depended on to withstand the stresses winds and other forces.

Use of tie-downs varies by state, state regulations and soil type. Local building inspectors and mobile and manufactured home builder associations are excellent sources for anchoring and tiedown requirement information. Use of that valuable information, along with insurance, is great methods for fully protecting a mobile home.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution,

whether in whole or in part, in any form of media or language; and no matter

what country, state or territory, is expressly forbidden without written consent

of Insurance Publishing Plus, Inc.

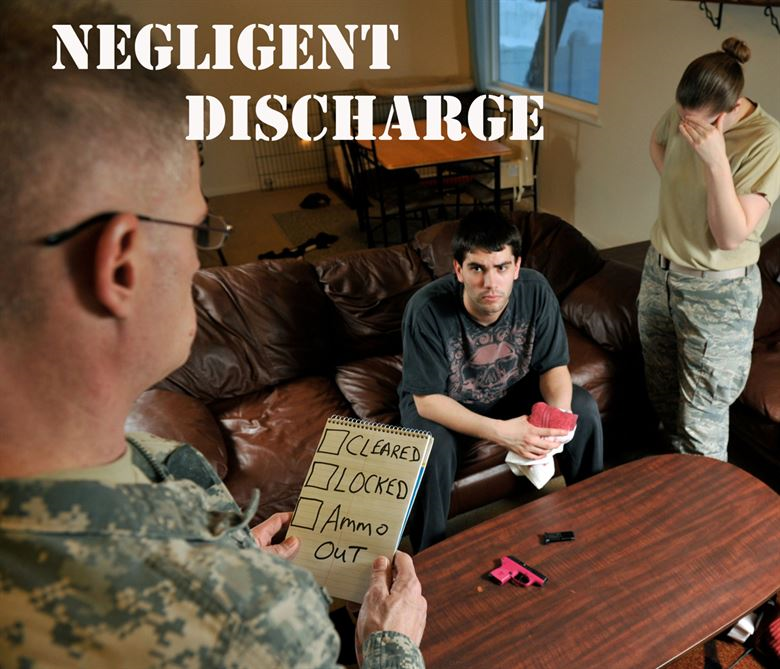

In 2010,

during a party that involved minors drinking alcohol, one guest was shot and

killed when a gun, being played with by its owner (another party attendee) went

off. The parents of the deceased sued the parents of the gun handler. The

latter requested coverage from their homeowner insurance company. The company

denied coverage and, eventually, a court ruled that no obligation existed under

the insurance policy. The company was released from the lawsuit.

Homeowners coverage, like other insurance policies, is

intended to protect against losses that are accidental. Often, accidental

losses can be readily determined, but incidents involving firearms are

complicated.

Accidental discharge of a gun can be a crime

When one

person injures another, both the act and the intent are considerations of

whether an incident is an accident. In the shooting incident mentioned above,

it was determined that the gun handler was guilty of negligently handling the

gun and was jailed. Since a court determined the incident was a crime, it did

not qualify as an accident. A loss caused by a crime is ineligible for

coverage.

When a

loss involves firearms, it is often treated far differently than other

circumstances. Consider the following:

Jim is

hosting a party at his house for a bunch of high school friends and Fran is one

of the persons attending it. Jim, well known to his friends as the group’s

clown, is fooling around with an item. Fran, who is nearby, is seriously

injured. Later, Fran’s family sues Jim’s parents and they file the lawsuit with

their insurance company.

Scenario

one – Jim recently became interested in tennis. He brings out a very expensive

tennis racket he just received. He brags about how light and powerful it is and

he demonstrates strokes. When he demonstrates a backhand, Fran is passing

behind him and she is hit, suffering a broken nose and several shattered teeth!

Scenario

two – Jim recently became interested in firearms. He brings out a very

expensive pistol he just received. He brags about how light and powerful it is

and he demonstrates how it is supposed to be handled. When he demonstrates how

to aim it, the gun fires and Fran is struck. The bullet hits and fractures her

shoulder.

In both

scenarios, the injuries are a result of Jim’s immature and careless action. In

both situations, no harm was intended. In both instances, Fran is seriously

injured. In all likelihood, the losses will not be handled similarly. A tennis

racket is a piece of equipment that is intended to be used for a particular

sport. It is used for hitting tennis balls and other uses are considered

unusual and, for the most part, not dangerous. This loss has a very high chance

of being treated as an accident.

A gun is

a weapon. It is used for both defensive and offensive purposes and, by nature,

is capable of extremely serious, often deadly harm. It is considered to be a

dangerous instrument. Therefore, the stakes are far higher whenever a gun or

other firearm causes a loss. In many instances, even when harming another party

is completely unintended, acts involving firearms also involve far more

accountability and may not be classified as accidental. In the shooting

scenario, the chance is very high that the loss would be denied.

Because of the danger inherent in guns, it’s important to be aware that losses involving them are often ineligible for insurance protection. That makes it critical that their ownership is treated seriously and every possible precaution against unintended injury be taken.

COPYRIGHT: Insurance Publishing Plus, Inc., 2016

All rights reserved. Production or distribution, whether in whole

or in part, in any form of media or language; and no matter what country, state

or territory, is expressly forbidden without written consent of Insurance

Publishing Plus, Inc.

I promise to never complain about doing laundry again!

Handling our many household chores is all about convenience. For many decades, the incredible washer and dryer power duo have made it possible for us to enjoy easy access to clean, ready-to-wear wardrobes. However, these appliances have a dark side that can result in serious loss, particularly dryers.

The United States Fire

Administration (USFA), a federal agency that collects and shares data on

fire-related losses, reminds us that dryers, while extremely handy, can also be

dangerous. In a recent agency report, fires caused by clothes dryers result in

losses of $35 million per year, nationwide. Let’s repeat that – $35 million in

dryer-related losses each and every year.

Preventing a home fire

According to the report,

such losses occur more frequently in cooler weather, occurs mostly in

residences and, for a bit of good news, most fires are limited to the dryer

itself. However, such fires can and do easily spread to other parts of an

apartment or home.

More than a third of

dryer fire losses are created by insufficient dryer maintenance and improper

use. Therefore, dryers, as a source of loss, are quite controllable by

homeowners. Here are some suggestions to help minimize dryer fires:

Properly and regularly clean out lint traps – that should include vacuuming out the area housing the lint trap too

Avoid putting items in a dryer which are more prone to igniting such as items containing foam (lined drapes, athletic shoes, bathroom rugs)

Remove lint that accumulates underneath and in areas outside of the dryer which is also sources of fire

Regularly clean out dryer vents. A thorough job is necessary to keep vents free of accumulated lint and, even more serious, bird or rodent nests

Do not overload dryers since fires are more likely due to restricted airflow and higher heat build-up

Make sure the dryer vent pipe is properly installed and is free of kinks (again, to avoid airflow restriction and heat build-up

Consider using a dryer that has a moisture sensor which can end dryer cycles with less of a heat build-up that is permitted by dryers that use thermostats

These simple few safety

steps are all that it takes to help avoid a potentially serious fire. Be clean,

be dry……and be smart!

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All

rights reserved. Production or distribution, whether in whole or in part, in

any form of media or language; and no matter what country, state or territory,

is expressly forbidden without written consent of Insurance Publishing Plus,

Inc.

If protecting one’s home isn’t complicated

enough, it appears that the soft, soothing glow of a candle’s flame may obscure

some dark problems. Specifically, the use of candles may result in:

reducing the internal air quality of your home

increasing the chance of fire losses

damages by particulate deposits on interior and exterior walls, carpets, furniture, appliances, window treatments, floors, and other surfaces

Further, the use of candles may

also contribute to health problems from inhaling particulate matter or

ingesting harmful chemicals.

Defining the Candle Problem

Today’s candles can be more of a hazard than an aid.

Actually, there are a number of

problems and they have been accentuated by a change in the market for candles.

The last few years have seen an explosive growth in the popularity of candles.

They are increasingly used for their traditional, decorative purpose, but the

true surge in use has been due to their being marketed as scented candles for

deodorizing and for a health-related purpose called aromatherapy.

In both of the above,

sales-boosting instances, candle-makers have had to offer products with more intense

scents. This is accomplished by adding scented oils into their wax mixture. The

increased oil content causes candles to burn improperly and generates a

substantially higher level of soot.

A Sooty Situation

It looks like soot, which is a

carbon residue produced by burning, can create a large, expensive problem.

Since soot is particulate matter that can be carried through the air, it can

seriously stain walls, carpets, and personal property. Studies show that

electronic and plastic components are also vulnerable to soot damage.

Unfortunately, soot produced by poorly burning candles bonds very strongly,

making it difficult to impossible to clean. Further, soot may contaminate a

home’s heating system, including ductwork. The soot can then be spread

throughout a home, creating widespread damage that is difficult to repair.

Property stained by soot may have to be cleaned by professionals and, often,

the property has to be replaced.

Troublesome candle ingredients

Do you know what’s in your candles?

You may have assumed that the only materials found in candles were the wick and some type of wax. Surprise! Here’s a list of ingredients which may either be found in a candle or maybe created during combustion:

Another surprise is that the candle-making industry is not required to tell consumers about the ingredients used in their products, including when a wick is used which contains a lead core.

Poor candle design or practices

Are candles with high flames or a lot of soot safe?

Besides the use of oils and

chemicals, candle-makers sometimes create problems because they commit other

mistakes. Candles may burn improperly (causing soot) because a candle’s wick

may be off-center or there may not be a proper amount of air in the candle

mixture. A candle may have a higher likelihood of causing a fire loss due to:

an improper candle mixture which results in intense heat or high

flames

improper holders (glass that shatters or spills flammable liquid)

wood holders that catch fire

flammable items imbedded in the candle mixture such as potpourri

Coverage Under

a Homeowner Policy?

Are you covered for losses started by candles?

Damage to a home or personal

property due to soot can create serious problems for both an insurer and a

homeowner. Losses involving soot can create thousands of dollars in damages.

Depending upon the details surrounding a loss and the wording of the particular

homeowner policy, coverage for the damage may not be available. Why? Because the source of loss might be considered the result of

pollution which may be excluded. Another reason for rejecting a claim

may be an assumption that the damage was gradual instead of sudden, so it

wouldn’t be considered accidental and sudden damage. A claim could even be

affected by the knowledge of the insured. For instance, even if the policy

covers soot-related losses, a claim could be denied if a homeowner knew that

the type of candle they used could cause damages.

Since the damage is caused by

matter that is invisible to the naked eye, it could be difficult to prove that

the loss was sudden. Tests can be used to determine the cause of stained or

discolored property, but the testing can be expensive and the cost may have to

be handled by the homeowner.

What To

Do?

It’s all up to you. You might wish

to ask more questions about the type of candles you use or curtail your use.

You can also discuss whether coverage is available under your homeowner policy

with an insurance professional. If you do use candles frequently, you may also

want to check your home thoroughly for any stains or discoloration, including

any contamination of your heating system.

COPYRIGHT:

Insurance Publishing Plus, Inc. 2016

All

rights reserved. Production or distribution, whether in whole or in part, in

any form of media or language; and no matter what country, state or territory,

is expressly forbidden without written consent of Insurance Publishing Plus,

Inc.

This article briefly discusses how a homeowner policy responds to

coverage for exchange students. Please be sure to read the companion article,

“Exchange Students – Automobile Coverage.”

You have an Exchange Student, Now What?

Note: Check

with your exchange student program coordinator to see what kinds of coverage

are automatically provided for the child. But don’t take anyone’s word; get

copies of documents that prove the coverage situation.

An exchange student in your care who is younger than 21 years is automatically insured under a homeowners policy, treated as if the child were a relative. An exchange student’s property is covered while located at or away from your home. Off-premises coverage is normally limited to 10% of your policy’s Personal Property limit, subject to a minimum of $1,000. On-premises, the policy’s full content limit is available. If your homeowner’s policy had a $70,000 limit for Personal Property, up to $7,000 would be available to handle damage or loss to an exchange student’s property while it’s away from your home, say while at a summer camp. Liability coverage that applies to your family also applies for damage and bodily injury caused by an exchange student who is younger than 21 years of age.

how to prepare for an exchange student.

If the exchange student is older than age 21, then the policy treats the student as a guest. A policy owner can volunteer to extend his insurance coverage to include a guest’s property while at your residence premises or even while you and the guest are at some other location. However, it is sometimes difficult to determine whether an older exchange student is a guest or a tenant – someone who is paying you a reasonable rent for staying in your home.

Hosting an exchange student creates questions you should discuss

with an insurance professional who can help make sure your coverage needs are

met.

COPYRIGHT: Insurance Publishing Plus, Inc. 2017

All rights reserved. Production or distribution,

whether in whole or in part, in any form of media or language; and no matter

what country, state or territory, is expressly forbidden without written

consent of Insurance Publishing Plus, Inc.

It’s quite likely that you face many demands…a job, family, hobbies, volunteer work, children’s school, and recreational obligations. Those items don’t cover chores, such as the lawn and garden, house cleaning, repairs and on and on. Like many of your peers, you might find that you just don’t have the time to get all of it done. Also, like many of your friends and neighbors, you may be “outsourcing” some of your responsibilities. Increasingly, people are hiring others to either assist or to take over duties such as:

child-rearing

gardening

decorating

housecleaning

laundry

grocery shopping

personal errands

child-transport

minor home repairs

lawn maintenance

meal preparation

exercise

While such help used to fall under the auspices of butlers, maids, and nannies, today, individual specialists are providing similar services on either a part-time or full-time basis.

Personal Services and

Personal Liability

Many service providers have insurance

When personal services

are provided by employees of a commercial business, such as a limousine

service, laundry service or a lawn care company, there’s generally no need to

worry about being held liable for injury to another person or for damage to

their property.

Example: The Burlies never had time to take care of their

lawn. As their grass grew thinner and the weeds spread, Mr. Burlie decided to

sign-up for the “Green Thumb” package from Lucy’s Lawn Services. One

afternoon, a Lucky Lawn specialist arrived at the Burlie’s home, unraveled a

hose and began to spray weed killer. A few minutes later, Stevie, who lived

several homes away from the Burlies, came rushing by on his skates.

Stevie didn’t see the hose until it tangled his wheels and sent him

headlong onto the cement sidewalk. In this instance, Lucky’s Lawn Services

would be responsible for the injuries.

However, as individuals

are hired by Joe and Jane America to perform personal services, the

responsibility for injuring other people or damaging the property of others may

begin to fall upon Joe and Jane. In these cases, will Joe and Jane have any

help in paying for damages or injuries?

Homeowners Insurance to

the Rescue

Homeowner’s Insurance

A person who employs the services of another may be held legally liable should the “employee” cause an accident. Can the average person who is guilty of nothing more than trying to make their lives a little less hectic depend upon their homeowner’s insurance for protection? Well, coverage depends upon the details surrounding an event. Generally, a homeowners policy will exclude coverage for losses that are related to the covered person’s (insured’s) business or when other coverage, such as workers compensation or disability insurance, should apply to the loss.

Handyman

Example: Molly Kelp really likes her neighbors’ son,

Peter, who is home from college. Molly knows that Peter is struggling for money

to keep attending school, so she occasionally hires him to do jobs around her

home and yard. One day, she asks him to trim the branches of a tree that is in

the front of her home. The branches are low enough to disturb traffic in the

street. Peter jumps down from the ladder he’s using for the job at the same

time that a car is passing by. The ladder tips over and crumples car’s hood as

well as smashes out the windshield. The driver slams on his brakes and is

severely cut-up in the process. In this case, Molly’s homeowner policy may

apply to the damage and injury caused by Peter. Why? Because the work was

strictly related to maintenance of Molly’s residence and premises. If Peter

caused an accident while carrying a ladder to paint Molly’s law office which is

housed in a converted bedroom of Molly’s home, the loss would be excluded from

her policy.

Do Your

“Homework” On Personal Services

If you’re not sure about

what happens when a person you hire causes a loss, you need to do your

homework. Discuss the details with an insurance professional and bring a copy

of your insurance policy. Between the two of you, you should be able to make

sure that your needs are covered.

COPYRIGHT: Insurance Publishing Plus, Inc. 2015

All

rights reserved. Production or distribution, whether in whole or in part, in

any form of media or language; and no matter what country, state or territory,

is expressly forbidden without written consent of Insurance Publishing Plus,

Inc.

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions