Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get DirectionsRenovating your home can be a great way to increase its value while improving your quality of life. However, it’s important to realize that it can impact your home insurance policy if you don’t work with your insurer before and after the work is done.

How Home Renovations Impact Insurance

When you purchase a home insurance policy, your insurer agrees to insure the home in its present condition and at its present value. If these factors change, you’ll need to inform your insurer and update your coverage to ensure your home remains properly covered at its current value.

Some home renovations also affect liability coverage. A new pool, for instance, increases the likelihood of accidents on your property and will likely raise the cost of coverage. However, if you don’t tell your insurance agency about the pool, your insurer can deny compensation for any pool-related accidents. On the flip side, safety features such as a new smoke detector system can lower the cost of coverage by decreasing the likelihood of accidents.

If you’re not sure how certain home improvements will impact your coverage, talk to your insurer before you start work. Bear in mind that your insurance agency will want to ensure you have needed permits and that the work is done by a licensed contractor. DIY jobs without proper permitting can result in your insurer revoking coverage.

Call TruePoint Insurance in Pooler, GA, for More Information

Want to find out more about home insurance liability coverage? Our TruePoint Insurance office in Pooler, GA, can answer any questions you have, help you review coverage options, and find home insurance that meets your needs without breaking your budget.

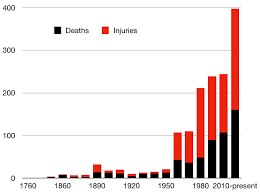

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection.

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection. industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

In part one of this article, we discussed the situation of properly classifying workers. In this part, we discuss a method for making that distinction.

In part one of this article, we discussed the situation of properly classifying workers. In this part, we discuss a method for making that distinction. another element is the nature of the work. Some businesses want to minimize both their tax liability and legal liability (and related payroll costs) by use of independent contractors. However, the situation can’t be a façade. If workers have an ongoing relationship with the applicable business because the work is normal for that business, likely the work involves employees. When the work is unusual for the given business and lasts for a short period, especially when it involves specialize labor or skills not existing in that business, the work likely involves independent contractors.

another element is the nature of the work. Some businesses want to minimize both their tax liability and legal liability (and related payroll costs) by use of independent contractors. However, the situation can’t be a façade. If workers have an ongoing relationship with the applicable business because the work is normal for that business, likely the work involves employees. When the work is unusual for the given business and lasts for a short period, especially when it involves specialize labor or skills not existing in that business, the work likely involves independent contractors.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security. Because of the position held by policyholder/insureds and insurance companies, the classification of workers is often in conflict as insureds desire liberal coverage and insurers wish to restrict protection to qualified persons. However, both parties are best served when worker classifications are clear. Premiums charged to policyholders are based on correctly recognizing the parties eligible for coverage. Proper classification keeps coverage affordable and makes the insurance process more efficient. Coverage involving employees should be connected to an applicable business that employs them. Coverage involving independent contractors should be connected to the contractors. In other words, they should secure their own, separate coverage.

Because of the position held by policyholder/insureds and insurance companies, the classification of workers is often in conflict as insureds desire liberal coverage and insurers wish to restrict protection to qualified persons. However, both parties are best served when worker classifications are clear. Premiums charged to policyholders are based on correctly recognizing the parties eligible for coverage. Proper classification keeps coverage affordable and makes the insurance process more efficient. Coverage involving employees should be connected to an applicable business that employs them. Coverage involving independent contractors should be connected to the contractors. In other words, they should secure their own, separate coverage.