TruePoint Insurance is one of Georgia�s fastest growing insurance agencies. We are affiliated with SIAA, a network of over 5,000 insurance agencies across the US, who by joining together have increased their strength and stability...

Broad Form (Homeowners Insurance Covered Causes of Loss: Broad Form)

The Broad Form is one of three ISO (International Organization for Standardization) use by the insurance industry to define which perils or causes of loss are covered. Generally, the Broad Form covers the perils covered by the Basic Form (see below):

I’ve heard that tragedy defines us. I disagree with that; it is how we as a group rise and address adversity that defines us. An excellent example is my grandfather’s generation. They’ve been referred to as the Greatest Generation, a fitting accolade to the group that defended our freedom and won WW II.

What is the great tragedy of our generation? Is it global warming? It could be the rise of terrorism! While I can’t answer the question, I do know that school shootings and other active shooter related incidents have to be somewhere in the mix.

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection.

The insurance industry is actively working to develop products that will protect businesses, schools and other government entities from gaps in current insurance policies. Professional liability policies were not designed to protect against active shooter risk or anything similar to that.

So what can be done and how do we do it? Products have been created and will continue to improve that will offer financial protection to entities that have been accused of failing to adequately prepare. But there is more.

Insurance companies seldom get the respect that they deserve; however, behind the scenes they are making a difference. The insurance industry is much more than a financial risk transfer vehicle, insurance companies are the leaders in making our world a safer place to leave. While most of us will never understand the significance, the insurance industry will lead America’s efforts as we deal with the risk of loss of life, mental trauma, and financial loss associated with active shooter incidents.

How? Who understands risk as well as the insurance industry? The better we understand risk exposures, the better we can prepare. The insurance industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

The insurance industry is working to make our world safer. If you are interested in learning more about the insurance industries role in managing active shooter risk you are more than welcome to contact us:

As we mentioned in part one of this discussion, a strategy for dealing with this exposure involves a significant amount of pre- and post-incident activity. Active shooter programs commonly involve the following:

Non-Insurance Services

Pre-event

Risk Assessment

Employee Crisis Training

During Event

Crisis Management

Second (Event) Responders (those who supplement initial, emergency action of fire, medical and police [first responders] and handle return services and site clean-up.)

Post-event

Counseling Services

Psychiatric Care

Public Relations Disaster Team

Investigation Assistance Funds (Rewards)

Expenses for additional, temporary security measures

Insurance Services

Liability Coverage for Lawsuits due to loss created by active shooting incident

Limits vary from $250,000/$500,000 up to multi-million dollar maximum

Business Income and Extra Expense

Limits vary from $1 million up to $100 million

Emergency medical care

Rehabilitation Expenses

Funeral and Burial Expenses

Marketing for the product targets those who are most vulnerable to this exposure such as Educational institutions, Entertainment organizations, Hotels, Healthcare providers, Religious institutions, Retail organizations, Shows (ex. Fairs, Trade Shows and Rodeos.)

Click here for Home Page

Return to Part 1

COPYRIGHT: Insurance Publishing Plus, Inc. 2018

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

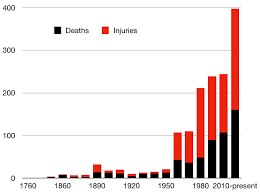

Headlines tragically remind us quite frequently that many aspects of our lives have become unavoidably dangerous. Sadly, this danger is due to the whim of individuals and access to weaponry. The deadly risk is the “active shooter incident.”

An active shooter incident describes a situation in which at least one person is actively killing or attempting to kill persons in a populated area. Naturally, as we are referencing a shooter, such incidents involve firearms.

Active shootings are becoming more common. Studies made by the FBI between 2000 and 2015 indicates annual mass-shooting events rose from 6.4 per year to 20 per year. Studies also show that most shootings take place within a business or school (educational) environment. The frequency of shootings is accompanied by, on average, an increase in the number of persons killed or wounded per event.

As with any other risk that becomes significant, it is very important to find a strategy to deal with active shootings. Insurance is among the tools helpful with both pre- and post-incident planning. However, much uncertainty exists regarding protection for active shooter losses.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

Confusion may also be caused by insurance policies via the silent coverage problem. An insurance form is considered silent when it neither specifically names nor excludes a source of loss, such as shootings. It can be chaotic during the time it takes to clarify coverage gaps.

The insurance sector has a reputation as being slow to react to change. Of course, speed is never at the level that most would wish when new coverage issues arise. However, the insurance market has been stepping up and addressing the serious active shooter exposure. While there is the option of trying to amend standard policies to add protection, other ways that coverage is being addressed are separate policies that supplement insurance protection with a variety of services.

Please see part two for more information on this issue.

COPYRIGHT: Insurance Publishing Plus, Inc. 2018

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc.

Do I need business insurance? Does your business have commercial insurance? Some businesses are required to have insurance, others are not. How do I determine where my business falls. If you are required to have businesses insurance, you likely know. A governmental body may require your business to have a license. If that’ the case, it’s very likely that you couldn’t get your license unless you had prior proof of insurance. Truckers, plumbers, insurance agents, and real estate agents are a few examples.

If I am required, what types of insurance will I need?

There is a purpose behind governmental units requiring businesses to carry insurance. They do so because of their charge to protect consumers. As a Commercial Liability Insurance result, when insurance is required, it is, most likely to be a Liability coverage. The two most common forms are General Liability (GL) and Professional Liability. Many contractors are licensed by the state. In Kentucky, this is done by the Department of Housing, Building, and Construction. Plumbers are governed by a subdivision of the department, the Division of Plumbing. The Division of Plumbing has as many requirements. The one we are focusing on is the requirement to provide proof of insurance. It is a state mandate that all Kentucky plumbers have in place a general liability policy. The policy must have a minimum limit of $250,000.

Many industries revolving around motor vehicles use a different form of liability insurance. One example is Truckers. Their liability protection comes from policies identified as Trucking or Non-Trucking Liability. They are very specific coverages that are part of the Commercial Auto Policies (CA).

Auto dealers, garages, and body shops are protected by two liability policies created specifically for them. Dealer customers test drive vehicles and there is a very high turn over. Garages test drive customer vehicles, some even tow the client’s cars. These are a few reasons this group needs specialized coverage. Garage Liability and Garage Keepers Insurance have characteristics that appear like a blended GL and CA policy.

Professional Liability Insurance has long been associated with services industries. It goes by many names; errors and omissions (E&O), medical malpractice, directors, and officers. This coverage protects businesses against claims of negligence. Kentucky Insurance Agents and Real Estate agents are two examples of businesses required to have E&O coverage.

Why are we still here if insurance isn’t required?

If anyone ever tells you that you don’t need insurance don’t ask why just run! I recently I saw someone involved in the insurance industry proposed the following absurdity. They suggested that risk change if your business operated online and didn’t have employees. Actually, they went as far as to say that such companies had little need for commercial insurance.

WHAT!

Be sure to get their E&O info before taking there advising.

Before deciding to waive the insurance coverage, step back. What could go wrong today and how will I pay for it. Reconsider all your risk. Think about the online company, the one that has no risk. The one that doesn’t need commercial insurance. a

Consider the following: Do you have customers, clients, consumers, or readers? If you answered no then are you really in business?

Could you make a mistake that would cause financial loss, or negative impact a customer? It is most likely insurable!

Could a vendor, affiliate, or other business relationship impact your business? Could one cause a temporary shutdown of your business? In most cases, you can protect yourself with insurance!

Ever heard of Cyber Liability? What exposures do you have when someone hacks into your system? Cyber risk can be defended.

Everyone has risks, even an online business. When you start to consider cyber exposures you very quickly release that this could be a very significant exposure. If you’re interested in reviewing your risk profile feel free to give us a all. (502) 410-5089. Some form of commercial insurance is needed by almost all businesses. That’s why it is so important that you find an insurance agency that you can trust. No insurance premium versus the option of no insurance company. When you have a claim, what is the highest the loss can be? When I do the math, those are odds that I don’t like.

give us a call, we’re TruePoint Insurance. An insurance agency that’s committed to doing insurance your way. We know our role, and it’s not to sell insurance. We help businesses like yours every day.

Garage operations are businesses that have hybrid coverage need. With such businesses, the lines between the general liability for the operations and the automobile liability exposures blur and overlap. A general liability policy does not provide enough coverage and a commercial auto policy provides too much. Fortunately, there is a way to properly handle this need. The Auto Dealers Coverage Form contains premises liability, products liability, automobile liability, and automobile physical damage coverage. Operations that should be protected by this policy include the following:

franchise and non-franchise auto dealers

truck dealers

motorcycle dealers

snowmobile and recreational vehicle dealers

new and/or used trailer dealers

vehicle repair shops

service stations

storage garages and

public parking places

Need help finding the right Dealer or Garage insurance?

The Auto Dealers Coverage Form is flexible, having the ability to cover a wide variety of automobile loss exposures. Besides covering vehicles that are owned by the covered business, it may also cover vehicles that are non-owned (rented or borrowed), trucks and other non-private passenger vehicles, trailers and mobile equipment. Coverage may even apply to vehicles that are privately owned by employees, but were involved in a work-related loss; says an employee who has a collision in his personal car while returning from picking up lunch for his boss and co-workers.

An Auto Dealers policy may also be written to customize how coverage applies to different types of vehicles. For instance, Joe’s Towing Service has a fleet of four tow trucks, as well as a sedan used by the owner. The towing service also does repairs and regularly has customer vehicles on their premises. Rather than having both liability and physical damage on all cars the services either owns or handles, Joe selects the following:

Liability and Physical Damage – for his two newer tow trucks and his sedan.

Liability only – for his two, older tow trucks

Physical Damage Liability only – for vehicles belonging to customers

Like other types of policies, an Auto Dealers coverage form also provides legal defense coverage. In other words, the policy handles the costs associated with defending the policy owner against claims and lawsuits. This protection does not affect the separate limits of insurance that are selected for the liability coverages.

COPYRIGHT: Insurance Publishing Plus, Inc. 2016

All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without the written consent of Insurance Publishing Plus, Inc.

Great Home Cooking, Bad Home Cooking, Little Middle Ground The same can be true with commercial insurance agents.

Factors Influencing Premiums

Obtaining insurance for a restaurant is fairly simple. However, finding the correct coverages at a reasonable price may be a bit more difficult. Different cuisines, Franchises versus Mom and Pop, and the processes utilized for cooking are just a few of the factors that may influence a restaurants premium. Other factors can have a more dramatic impact on premiums. Alcohol sales, entertainment (such as live music or karaoke) and dance floors may make it harder to find coverage, which by default will push the cost of coverage higher.

Restaurant Safety

Don’t forget liquor liability coverage

Cooking areas are required to have automatic fire extinguishing devices. Hoods and filters must be in place if grills and deep fat fryers are used. Additional requirements will be fuel shut-offs, hand-held fire extinguishers, as well as receipts providing proof that inspections and hood cleaning are being performed as required.

Restaurant Safety Starts in the Kitchen

Minimum Coverages

At a minimum, the following factors must be considered before purchasing a commercial insurance policy for a restaurant:

Property Coverage-building, equipment, and inventories

Autos

All vehicles owned by the businesses

Employee vehicles should be covered by a hired and non-owned vehicle policy if they are used in business activities (even it’s occasional)

It is important that you make your agent aware of any vehicle, owned or non-owned, that is used for delivery

Business Income –In the event, your business is temporarily shut down due to a covered cause of loss, restaurants with business income coverage can access their insurance policy for loss of income.

This quick summary of restaurant insurance is not meant to be inclusive, nor is it a one size fits all. Each restaurant is unique and insurance requirements vary. If you would like additional information regarding a restaurant in Kentucky Tennessee or Indiana, contact a TruePoint Insurance Restaurant Specialist at info@truepointgroup.com or visit our website at www.insuringky.com

The Greek historian Herodotus is credited with the saying, “Neither snow nor rain nor heat nor gloom of night stays these couriers from the swift completion of their appointed rounds.” His words were describing the dedicated work ethic of the Angarium, Royal mounted couriers in ancient Persia.

USPS Rural Letter Carriers can get Auto insurance at an affordable price. It’s not as difficult as you might think.

Two thousand years later the famous words of Herodotus are now used to accurately describe another group of couriers, the US Postal Service. Granted lots have changed over two thousand years. Technological advancements and modern transportation systems have simplified the process of accurate and timely delivery of mail. However, not all advancements have made the life of mail couriers easier.

For most of us, buying auto insurance is a rather simple process. However, for independent or rural mail carriers, obtaining auto insurance is much more complicated. Finding an agent or broker that is willing to offer mail carrier insurance is a significant challenge. It gets worse; many times those that think they have coverage for their USPS vehicle find out when attempting to file a claim, that they have purchased a policy that does not cover the vehicle while on their route.

The personal cars of rural letter carriers must be covered by a commercial or business policy. More specifically mail carrier insurance. While that doesn’t sound like it would create a big problem, it is.

Reasonably prices auto insurance is available for Rural Letter Carriers.

The world we live in postal carriers must still brave the snow and rain. But that’s not their biggest problem. Getting through to an insurance agent that a standard personal auto policy will not provide coverage. The same is true for the standard commercial auto insurance policy, USPS letter carries are not protected.

Still, the mail must go through. mail carrier insurance for USPS rural carriers presents a significant problem. However, the transfer of risk doesn’t have to be difficult, nor should rural delivery contractors worry if they have a policy that will provide adequate coverage in the event of an accident. Visit our website at www.insuringky.com or call and speak with a TruePoint agent for a quote that will provide you with USPS vehicle insurance.

TruePoint Insurance Group, LLC

6287 Taylorsville Rd. Fisherville, KY 40023

6287 Eagle Lake Dr Lawrenceburg, KY 40342

Pooler, Georgia Location to be announced soon

Kentucky and Indiana Rural Letter Carriers: (502) 410-5089

Georgia and South Carolina Rural Letter Carriers: (912) 330-1265

For lawn care and landscaping businesses in Kentucky, the winter months represent a time to play catch-up. During this period when it’s tough to find ways to make a buck, why not take the time to make sure you’re not leaving money on the table by getting a comparison quote on your business insurance. Even more important, take the time to do a complete and thorough review of your insurance coverage. While this may not have an immediate impact on your bottom line, it may someday have a very significant impact on the profitability of your operations. With that in mind we decided to take some time to share with you some of our thoughts regarding insurance and risk management for lawn care businesses.

Liability Coverage Can be purchased in various amounts. You are most likely to have a policy which provides liability limits of $1,000,000 per occurrence and $2,000,000 aggregate.

If you have anything less than this we would encourage you to reconsider. The savings associated with reducing coverage below these limits very seldom makes sense.

Property Coverage

Buildings Even if you don’t own a building you may still have exposure. Your policy should provide coverage for property that you rent from others.

Equipment Make sure that the limits for your property: mowers, trailers, etc. are in line with the current market, too low and you will pay the difference out of pocket, too high and you are already coming out of your pocket.

Scheduled Equipment Each insurance company has their own rules, but it’s worth checking to make sure that every item you want covered that has a value greater than $2,000 is scheduled and listed on your policy. This is opposed to having those items covered in the unscheduled portion. First off the rates for scheduled are lower than unscheduled. More importantly carriers have a limit which they use to cap unscheduled items, typically around $2,000.

EXAMPLE: Last year ABC Mowing purchased a used 72” Scag Turf Tiger for $12,000 The mower is being covered but is not specifically listed in their policy. The equipment was stolen and they are now dependent on the proceeds from their insurance claim to replace the lost mower. As unscheduled equipment, ABC Mowing will be limited to the $2,000 limit for unscheduled equipment, and before they get that they will be faced with whatever deductible is in place. In their case it was $1,000, leaving the company with only $1,000 to replace a $12,000 piece of equipment.

It would be one thing to find you had this coverage in place and although you are not happy about it, you were getting what you paid for. However in the scenario above ABC Mowing was actually underinsured and overpaid.

Commercial Auto Do you need a commercial auto policy or is your personal policy enough? Good luck at getting an answer on that one. Generally speaking, personal auto policies don’t cover autos while performing functions that relate to business. However commercial auto policies will cover autos while being driven for personal use.

Better Coverage Commercial auto policies generally have much higher limits than a personal policy. Given the litigious society that we live in, you must ask yourself, is my auto insurance putting my livelihood at risk?

The cost will most likely be less than you think We write a lot of first time commercial auto policies, replacing personal policies that just aren’t adequate. Almost always the customer has significantly better coverage and the prices only slightly higher or even less than where they started.

Caution: You may ask, “If I am in an accident how will anyone know I should have a commercial policy?” Do you have your business name, phone number, etc. on your vehicle? I’m not sure, but I am guessing that the attorney representing the other driver will notice that trailer with two mowers, five weed eaters, or whatever other tools you might be hauling. Maybe not! What I do know is, that unless you have actually considered a commercial quote you cannot make the decision.

TruePoint Insurance Group, LLC

6287 Taylorsville Rd.

Fisherville, KY 40023

(888) 706-5423

TruePoint Insurance Group, LLC is not licensed to practice law, nor can it provide legal counsel. This summary is not intended as a legal opinion. We cannot warrant that the opinions and representations provided in this summary are accurate. TruePoint Insurance Group, LLC has provided this summary of the Virginia Graeme Baker Act for your awareness. The summary may or may not identify your requirements as a pool or spa owner. If you own a pool or spa you are advised by TruePoint Insurance Group, LLC to refer your specific situation to legal counsel.

Regardless of the business, you’re in, it is likely, that you will need general liability coverage. Commercial General Liability (CGL) protects your business against claims made by third parties.

At times justifying insurance can be a challenge. Customers are not buying a commodity or a product. Many will classify insurance as a service. But the truth is, insurance is not a commodity, product or service. The insurance transaction is very much one-sided. The insurance company gets your money. As a result of the transaction, the consumer gets nothing more than a promise.

When you buy the insurance you are actually buying a promise. You exchange an insurance premium, for a promise of indemnification.

Liability insurance cost; the cost of staying in business

The value proposition for liability insurance is driven in large part on MAGNITUDE! Today seven-figure liability claims are not unheard of. Magnitude is the reason that your Commercial General Liability policy is essential. It should be a major component of your risk management plan.

CGL Insurance provides very broad coverages, but it comes with many exclusions. Automobiles; auto liability is covered under the Commercial Auto Policy. Also Professional Liability insurance, which comes under various names. E&O, D&O and Medical Malpractice are few. There are other professions that need liability policies. Policies specifically designed for the unique exposures that they face.

Professions that work with customers vehicles have specific liability insurance needs. Mechanics, auto body repair shops, and other’s need what is known as Garage Liability Insurance.

Vehicles not owned by the insured are not covered by either the CGL or the Commercial Auto Policy. The Garage Liability Policy fills this gap, providing the insured with coverage for incidents that occur on the premises. On-premises is key. It is important to remember that this coverage does not extend beyond the place of business.

Garage Liability is often confused with Garagekeepers and vice versa

Earlier we noted that Garage Liability covered on-site incidents. Does your business take customer vehicles on test drives? Do you drive customer vehicles to other locations? How about pick-up and delivery of customer vehicles? If your businesses drive customer vehicle off premises, you need a Garagekeepers policy. For more information on Garagekeepers Coverage forms see:

TruePoint’s on target review of Garagekeepers Coverage.

Garagekeepers or Garage Liability, as clear as spent motor oil

Business Liability insurance can get confusing. That’s why it is important for business owners to do some work on their end. It’s wise to invest some time on the front-end finding a good agent. Working with an independent agent increases your chance of success.

Working with an independent agent is even more important for businesses. The group combines to write nearly 85% of the insurance written in the US. 85% of the market makes it difficult for anyone other than an independent to agree their case. Garage Liability insurance coverage.

Identifying the right independent agent might be a little tough. Don’t be afraid to quiz them. Use your understanding of General Liability, Garagekeepers, and Garage Liability coverages. Put prospective agents to the test by asking them to suggest coverages.

The finish line is in sight. Choose the right path for you and your business to secure the necessary coverage.

Don’t feel bad if you’re still feeling a little confused. Many in the insurance industry have trouble with this topic. Who needs Garage Liability?

Garage Liability……working at your garage

Garage liability covers your customer vehicles. This coverage will not cover you if the vehicle leaves your place of business. Damage that occurs offsite will not be covered. Drive, tow or levitate the car to another location. It doesn’t matter, damages will not be covered. It is not uncommon to see Garage Liability policies with Garagekeepers.

Garagekeepers……keep the Garage Liability, you will likely need it too

Garagekeepers coverage picks up some essential coverage not included with the Garage policy. Collision is the primary addition, protecting the garage for off premises accidents. It also adds a few other exposures that would include, fire, theft, vandalism. Garage liability is seldom used without an associated garage policy.

Who needs Garagekeepers? And who needs both…

CAN YOU HAVE BOTH?

Yes, you can have both. And it’s not uncommon. If your business falls into one of the following classes it is highly likely that you should have one if not both of the Garage coverages:

Contact

Contact

Email an Agent

Email an Agent

Click to Call

Click to Call Get Directions

Get Directions

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection.

Tragedy is often the precursor of innovation. It certainly was during WW II. It also drives changes and the creation of new products in the insurance industry. The insurance sector exists because individuals, businesses and other entities have a need to transfer risks to another party. Increasing active shooter incidents in recent years and the corresponding legal actions have created demand for products that can provide financial protection. industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

industry will over time and after numerous assessments develop standards that when deployed will ward off many would be active shooters. They work for insurance companies will also work to reduce the after effects and of course provide financial relief.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

First, there is customer expectations. Insurance consumers may be under the impression that damage and injury created by shooters are covered. Second, the insurance market is fragmented over the issue depending upon how incidents are interpreted. Coverage may be sought from existing policies that individuals, commercial or non-profit entities may already carry, including General Liability, the Liability portion of Homeowners, or Workers Compensation. On the other hand, responsibility for harm due to a shooter may need to be covered by a form of professional liability policy as the obligation to protect against shootings may be considered as a failure to provide adequate security.

insurance needs.

insurance needs.

Garage liability covers your customer vehicles. This coverage will not cover you if the vehicle leaves your place of business. Damage that occurs offsite will not

Garage liability covers your customer vehicles. This coverage will not cover you if the vehicle leaves your place of business. Damage that occurs offsite will not